Sample application for social deduction for education. Education Tax Credit Information

Read also

Article navigation

The state is constantly trying to support those who educate themselves and develop their children. To do this, you can return funds paid for training income tax, withheld from income.

Personal income tax refund for education – what is it?

These are tax deductions social type, compensated primarily for “social” type taxes - such as medical care, education, and the purchase of health insurance. In other words, a tax deduction for education is a tax benefit received for social expenses.

Unlike the standard compensation, which is issued to the father or mother of a minor and is paid at the workplace, this compensation is only valid if the income tax for training has already been paid. Compensation is prescribed in Article 219. Tax Code of the Russian Federation.

The country's legislation does not offer a choice between a minor and a deduction for education. You can apply for both types of compensation.

For example, if a parent pays for his minor to visit a private kindergarten, then he can apply for both types of benefits. If problems arise with this, then you need to contact the tax office.

These compensations differ significantly in the receipt of funds, methods of registration, as well as in amounts. In addition, if standard deductions are taken by both parents and at the place of work, then To apply for social deductions, you will need to comply with the following rules:

- The deduction is issued not when the payment was made, but after the year in which the payments were made.

- Unlike standard deductions, the application must be submitted not at the place of work, but at Federal Tax Service. Although here citizens have little choice.

- The amount for the time while the citizen had the right to compensation, but did not draw up documents, is paid in a lump sum.

Who is eligible for the benefit?

You can receive compensation as follows: the students themselves, so relatives of the child who pay for his services, right down to his brothers and sisters. To do this, it is enough to issue face-to-face contract. They can do this:

- Parents of the child who has not reached 24 years of age.

- Guardians of a minor.

- Also, if guardianship has ended, but the guardian wants to pay for the services, this can be done for a child under 24 years of age.

- This can be done by a person for both half and full sisters and brothers under 24 years of age.

If a standard benefit is issued to both parents, then a social benefit is issued to only one of them, and not necessarily to the one who paid for the service.

The Ministry of Finance has an explanation on this topic. So, if both parents are married, then everything they have is considered joint property. Therefore, if one of them paid for the services, then with his consent, compensation can be issued by the second parent.

Age and duration restrictions

Let's decide on age restrictions. If you have paid income tax for your education, then you will be compensated for it at any age and in any form, be it part-time or even evening.

Let's decide on age restrictions. If you have paid income tax for your education, then you will be compensated for it at any age and in any form, be it part-time or even evening.

With children, everything is a little more complicated - you can return the tax on them before their due date. coming of age, or until 24 years old, if the child is studying at full-time. If a person is under former guardianship, then the guardian who wants to pay for his education can also receive compensation up to 24 years old.

Period for which funds can be returned

The law states that the person applying for the deduction can apply for the benefit for the entire period of time during which the training takes place, up to the academic leave. Moreover, for the parent the deduction will operate as follows:

- If the graduate is not yet 24 years old, then the tax will be provided Until the end of the month.

- If this year he will be 24 years old, then the tax will be provided until the end of the year.

You must apply for compensation after the year in which the payments were made has passed. If training takes place over several years, then documents are submitted to the Federal Tax Service over several years, or once in all years.

If for some reason the taxpayer did not have the opportunity to return the tax immediately, this can be done within 3 years after the service has been paid for.

If you apply to the Federal Tax Service in 2018, then you can receive compensation for 2015, -16 and 17. Moreover, it does not take into account whether your child has finished gnawing on the granite of science and how old he is. For example, if a child has already turned 25, then you can get a deduction for those years when he was already studying, but he has not yet turned 24. Of course, if you have kept the receipts for that.

How much can you get?

Compensation is provided only to a working family that pays for a child’s education, not who has reached 24 years of age and is engaged in full-time education. Such a family can receive compensation for the income tax paid, but the amount spent on education should not exceed 50,000 rubles. That is, the annual personal income tax for each child cannot exceed 6500 rubles.

In this case, a deduction can be provided for staying in kindergartens, private and municipal schools, colleges, universities, and even courses. In this case, an agreement must be concluded between one of the parents and the educational institution. And of course, the educational institution itself must have a license for educational services.

To receive the funds listed above, you should go to the Federal Tax Service at the end of the school year. In this case, the following conditions must be met:

- The child for whom compensation will be received must not be over 24 years old. In addition, he must undergo full-time training only.

- It is not a third-party organization that should pay for your studies, but one of the parents, or both parents alternately. This cannot be done by any company, enterprise, or especially a charitable foundation.

- In order to receive compensation, the parent must be officially employed and, accordingly, paid income tax. Those people who do not work cannot return the tax.

The total tax deduction provided for each child is equal to the amount that the family paid for his education for the year. That is, in fact, funds spent on studies are not subject to personal income tax. However, there are certain restrictions that apply to the amounts. So, you will not receive more money than you paid for taxes.

Deductions for a calendar year could not exceed:

- 50,000 rub.., which were spent by parents on studies.

- 120,000 rub.., paid for the education of a sister or brother.

For example, if a family spent 70,000 rubles on study in a year, then compensation will be returned only from 50,000 rubles. To calculate compensation you need to do the following:

50,000 x 13% = 6,500 rubles.

Maximum received for children:

- 6,500 rub. – for one child.

- RUB 15,600 – for a brother or sister under 24 years of age.

To receive personal income tax, it does not matter for which years of study you paid the funds - the actual date of payment is important. Compensation is paid from wages– winnings do not participate in the distribution of benefits.

Example of calculating deduction for a child

Let’s assume that the daughter of a certain Lyudmila entered a master’s program in 2015, where she needs to study for two years. For a year in educational institution you need to pay 100 thousand rubles, but the daughter’s father pays the entire amount at once for two years. In 2016, Lyudmila decides to apply for compensation and, having collected the paperwork for registration, submits them to the Federal Tax Service. At the same time, her husband’s salary is 40 thousand rubles per month.

Since the studies were paid in full for 2 years, the amount of payment for which compensation can be received is 50,000 rubles, and not 200,000 rubles, as the father paid for it (we take into account the minimum specified by law). Therefore, when calculating the return, we consider this:

50,000 x 13% = 6,500 rubles

But the employer took the following personal income tax from Lyudmila’s income:

40,000 x 12 (months) x 13% = 62,400 rubles

It turns out that Lyudmila will receive compensation equal to 6,500 rubles, since this amount does not exceed the maximum allowed by law. And I could get 13,000 rubles if I applied for the benefit for 2 years in a row.

By paying tuition for a child once, the parent has lost the maximum deduction. Therefore, for those who pay for study, it is more profitable to divide the amount into parts and spread it over several years of study.

How to apply for a benefit

When applying for a benefit, the taxpayer applies to the Federal Tax Service at the place of his stay or residence. For this:

- The education of your son or daughter is paid completely or by semester.

- When the school year in which the parent paid for the child’s education ends, the papers collected for registration are provided to the Federal Tax Service.

- After the Federal Tax Service has reviewed the papers, compensation is transferred to a bank account or card. Another option – funds are credited towards payment of future taxes.

Compensation will be transferred only after the taxpayer applies to the Federal Tax Service. If you do not want to wait until the end of the year, you can apply for benefits at your place of work by writing a corresponding application.

When applying for benefits from an employer, the following applies:

- The Federal Tax Service is asked to confirm that the taxpayer wants to confirm his right to benefits. The list of documents for application is specified by the tax office.

- Within a month After the application, a corresponding document is issued.

- The person submits the confirmation paper to the place of work. An application for early payments is being written.

- At work, personal income tax is calculated taking into account benefits. In this case, funds are paid not once a year, as in the tax service, but every month.

Papers for registration of deductions

All papers collected by a person must be provided in the form of copies, but originals will also be needed. When sending them to the Federal Tax Service by mail, you must first have the documents certified by a notary.

Of course, sending a letter by mail is more convenient - you do not need to visit the organization in person. But if you are applying for benefits for the first time, then it is better to visit the Federal Tax Service in person - if one of the papers is missing, you will know about it immediately.

When making a deduction for last year The following papers are collected:

- An application filled out in free form. The tax amount and transfer method are specified.

- 3-NDFL.

- 2-NDFL, which is taken at the workplace.

- Study contract indicating the license of the educational institution, price and form of training.

- Receipts paid by the child's mother or father.

- Document for the child.

- Details for which the tax will be refunded.

- If the agreement does not contain information about the license, then a copy of it is needed.

- Also, if the document does not indicate that the child is studying full-time, then a corresponding certificate is needed.

- If the benefit is provided by the mother and not the father who paid for the service, then a marriage certificate will be required.

- If the services are paid for by the guardian, then the decision of the relevant body is provided to the Federal Tax Service.

Papers for filing with the tax or Federal Tax Service are updated annually. The same applies to receipts - they must be new every time. Well, the information that your child is still studying full-time should be updated every year.

Deadlines have limits:

- The decision is made quite quickly, within just ten days, but some time may be needed for a desk audit, which can last up to three months.

- When a decision on the case is made, the applicant will be notified within 5 days.

- If the paperwork is completed correctly, the money will be transferred to the card within one month.

Registration of 3-NDFL

Before visiting the Federal Tax Service, fill out form 3-NDFL using certificate 2-NDFL taken at the place of duty. It includes several pages that need to be filled out correctly, and due to the fact that the tax office introduces something new into it every year, you cannot rely on forms for previous years.

It can be obtained and filled in one of the following ways:

- Private online services that are not very welcome by the Federal Tax Service. In addition, this service is paid. Most often, the tax office offers its services for filling out in real time - for example, “Taxpayer Account”.

- On the Federal Tax Service website there is special program, free to download. When filling it out, some nuances are indicated - for example, if you enter the information incorrectly, or do not enter it at all, the program will indicate this to you.

- The last option involves visiting the organization in person. Here you can take a blank form and fill it out on the spot.

When preparing the document, the following nuances are taken into account:

- Federal Tax Service number where the document will be sent. To do this, you should take care of the details in advance. But! There is a list on the tax website from which the desired organization can be selected.

- Sections such as full name, tax identification number, data from your personal account and Russian code must be filled out.

- The form contains the address of residence and OKTMO - this code is not on the website, but if desired, it can be easily found on the Internet.

- Information about the organization where the employee received wages is recorded. In the “Income” section, select the number 13, that is, thirteen percent taxation. If there is paid leave, the code 2012 is prescribed, if there is a salary - 2000 rubles. The amount that became the total for all income must coincide with the number on the certificate from the place of work.

- If the benefit is issued specifically for study, then this is the section that needs to be selected. And also indicate the real amount.

When filling out the program from the Federal Tax Service, the person who decides to return the funds has the opportunity to edit the document and print it at home. After filling out the form, you need to write a statement indicating the refund amount that you have calculated.

Paperwork - for whom and why

Let's figure out who and how documents are drawn up.

The contract is for the mother, the payment is for the son

In this turn of events, the deduction will not be paid, due to the fact that both papers are issued only to the parent.

The contract is for the son, the payment is for the mother

The same situation occurs when the benefit will not be paid due to the fact that both papers are issued in the name of the mother or father.

All papers are for my son

The tax office will 100% not pay compensation and will be right, based on Letter of the Ministry of Finance dated October 28, 2013 No. 03-04-05/45702.

Example of compensation for personal training

A certain Ivanova paid 60,000 rubles for a higher education institution. Her income for the year at work was 480,000 rubles. (40,000 x 12). The income deduction for her amounted to 62,400 rubles (480,000 x 13%).

Let's calculate the deduction:

Since Ivanova paid 60,000 rubles for her training, the refund amount will be 7,800 rubles (60,000 x 13%). And if the personal income tax was paid in full, then Ivanov can receive the same full amount.

Example for children studying full-time and part-time

Let's look at another example. Let’s assume that the same Ivanova has three children, and she paid for them as follows:

- For a senior who is studying full-time, 70,000 rubles were paid.

- For the youngest in private garden it took 40,000 rubles.

- I had to pay 60,000 rubles for my daughter in absentia.

At the same time, Ivanova’s total annual income was 480,000 rubles (40,000 x 12). At her place of work, Ivanova was charged 62,400 rubles (480,000 x 13%). Let's calculate how much was paid for compensation.

For each child in this family, personal income tax will be calculated differently:

- So, for a senior you cannot receive more than 6,500 rubles, since the benefit is issued not for the amount that was paid for him, but for 50,000 rubles.

- For the youngest, the amount will be less - 5200 rubles. (40,000 x 13%).

- As for the daughter, she is not entitled to benefits at all, since this form of education is not paid for.

Total for all children is 11,700 rubles.

Example with multiple compensations

Ivanova, in addition to her own studies for 80,000 rubles, also paid for medicines for her husband for 60,000 rubles. At the same time, her income did not change and also amounted to 480,000 rubles. in a year. The tax has not changed either, which is still equal to 62,400 rubles.

Calculate compensation:

In total, Ivanova paid 140,000 rubles for her studies and medications. But she cannot receive compensation for this exact amount, since the maximum by law is 120,000 rubles. Therefore, the maximum benefit returned to Ivanova is 15,600 rubles (120,000 x 13%).

Features of applying benefits

There are some nuances that are important when applying for benefits. Eg, you need to pay attention to the form of training when applying for compensation, since the Federal Tax Service will only allow in-person forms.

Only the parent, or both mother and father in turn, have the right to pay for the education of children - When paying by outside organizations, the deduction will again not be paid.

And of course, in order to get finance, you need to be officially employed, and pay payroll taxes to the state every month.

We also recommend watching a useful video about tax deductions for education with examples of calculations:

Russia, like other countries, is trying to support its citizens in every possible way. For example, here you can apply for a so-called tax deduction. It is provided for certain expenses. Today we will be interested in documents for tax deduction for education. In addition, it is necessary to understand when a citizen can demand certain money from the state. What do you need to know about the tuition deduction? How to register it? What documents may be useful in this or that case?

Where to go

The first step is to understand where to go to bring your idea to life. In 2016, tax legislation in Russia changed slightly. Now, according to the law, you can apply for various types (for treatment and study) right at work. What does it mean?

From now on, documents for tax deduction for education are accepted:

- in tax authorities;

- at the employer;

- through the MFC (in some regions).

The first scenario is most common. However, the list of documents attached along with the application does not change. He always remains the same.

Tuition deduction is...

What is a tax deduction for education? If a person paid for educational services, he is entitled to reimbursement of 13% of expenses incurred. This opportunity is spelled out in the Tax Code of the Russian Federation, in Article 219. The return of part of the money spent on education is called a tax deduction for education.

The deduction is part of the income that is not subject to taxes. In other words, in Russia you are allowed to reclaim tax on your study expenses. Accordingly, 13% of educational expenses for yourself and your children can be returned if you have income subject to personal income tax.

Who can I get it for?

Under what conditions can I submit documents to receive a tax deduction for training in a particular organization?

Currently, it is allowed to reimburse expenses incurred for studying:

- myself;

- children;

- brothers and sisters.

In this case, you will have to comply with a huge number of conditions. The recipient can only be the one who paid the money for study. As already mentioned, a citizen must have official work and income taxed at 13%.

When to make a deduction for yourself

As a rule, there are no restrictions on taking deductions for your own education. This is the simplest scenario. Among the main requirements in in this case highlight:

- Availability of official income. However, it must be subject to a 13% tax. Thus, an entrepreneur working with the simplified tax system or a patent cannot return money for training.

- Payment has been made educational services in official institutions. For example, studying at a university or driving school. Courses and trainings are not considered training.

I guess that's all. If these conditions are met, you can collect documents for a tax deduction for education. Distinctive feature receiving money for one's own studies is that the form of education does not matter. A person can study both full-time and part-time, evening or any other department.

Amounts of deduction for yourself

How much money can you get back for your own studies? By law, you can count on 13% of expenses incurred. But at the same time, there are some restrictions in Russia.

Which ones exactly? Among them are the following features:

- You will not be able to get more tax paid back. Only income tax is taken into account.

- The maximum deduction for training is 120 thousand rubles. At the same time, you can return no more than 15,600 rubles in a given year. This limitation is related to deduction limits.

- The current limitation applies to all social deductions. This means that for training, treatment, and so on, you can demand a total of 15,600 rubles per year.

In fact, everything is not as difficult as it seems. What documents for tax deduction for education will be required in this case?

Receiving a deduction for yourself

The list of papers is not too extensive. However, this scenario involves the least amount of paperwork.

Among the documents necessary to implement the task are:

- the applicant's identification document (preferably a passport);

- service agreement with educational institution;

- income certificate (form 2-NDFL, taken from the employer);

- application for a deduction;

- institutions (certified copy);

- 3-NDFL;

- payment slips indicating the fact of payment for educational services;

- details for transferring money (indicated in the application).

In addition, if you need a tax deduction for studying at a university, the documents are supplemented with accreditation of the specialty. All listed papers are submitted along with certified copies. Receipts and cash orders indicating the fact of payment for training are given to the tax authorities only in the form of copies.

Conditions for receiving a deduction for children

When and how can you apply for a tax deduction for children’s education? To do this, you will also need to follow a number of rules. Which ones?

To apply for a tax deduction for a child’s education, you must meet these criteria:

- children under 24 years old;

- children study full-time;

- payment for educational services is made by the parent;

- The agreement with the institution is signed with the legal representative (mother or father) of the child.

It is important to remember that you can get back no more than 50,000 rubles for one child. For the year the amount is 6,500 rubles. There are no further restrictions provided by law.

Documents for deductions for children

To reimburse expenses for a child’s education, it is necessary to prepare a certain package of papers. There are more of them needed than in the previously proposed list.

Documents for a tax deduction for a child’s education include: famous list papers In addition, it is complemented by:

- child's birth certificate (copy);

- student certificate (taken from the educational institution);

- a copy of the marriage certificate (if the agreement is concluded with one parent, and the deduction is issued to the other).

That's all. In addition, tax authorities may request a copy of the identity card of a child over 14 years of age. This is a normal phenomenon and there is no need to be alarmed. There is no need to certify a copy of your passport.

Conditions for receiving a deduction for brothers and sisters

As it was emphasized earlier, a citizen can return part of the money spent on the education of a brother or sister. This is a rather rare phenomenon, but it does occur in practice. The list of documents for tax deduction for education will be supplemented with several more papers. But more on that a little later. First, you will have to find out when a citizen has the right to reimbursement of expenses for the education of a brother or sister.

The conditions for receiving a study deduction in this case will be as follows:

- sister or brother is under 24 years old;

- the person is a full-time student;

- the agreement is concluded with the applicant for the deduction;

- all payments and receipts indicate that it was the applicant who paid for the training services.

What restrictions will apply to refunds? Exactly the same as in the case of deductions for children’s education.

Documents for deductions for brothers' studies

What papers will be required in this case? How is the education tax deduction processed? What documents are needed if we're talking about about a brother or sister getting an education?

The previously listed list of papers (for yourself) is supplemented by the following components:

- own birth certificate (copy);

- birth certificate of the person whose tuition the applicant paid for;

- student certificate (in original).

Nothing more is needed. In exceptional cases, you will have to submit any documents indicating a relationship with the student/pupil. But this is an extremely rare occurrence. Birth certificates are sufficient for the tax authorities.

Return period

The documents required for a tax deduction for education in a particular case are now known. A complete list of them has been presented to your attention. But there are still important unresolved questions.

For example, for what period are deductions allowed in Russia? How long is the statute of limitations for filing a claim? How long does it take for tuition tax credits to be refunded? You already know what documents to bring with you. But it is important to remember that the application can be submitted no later than 3 years from the date of certain expenses.

This means that the statute of limitations for filing a corresponding request is 36 months. In this case, the right to receive a deduction appears only in the year following the one in which the payment for services occurred. If a person paid for his studies in 2015, demand a refund Money allowed only in 2016.

In addition, you must remember that you can apply for money until the established limit is completely spent. Until the citizen has exhausted social deduction for training, amounting to 120,000 rubles, he is able to demand money from the state for appropriate expenses.

Can they refuse?

Can the tax authorities refuse this payment? Quite. Sometimes the population is faced with situations in which the response to a request is a refusal. This is normal.

What to do if you were unable to obtain tax deductions for education? What documents and where should I take them? In this case, it is recommended to study the reason for the refusal to refund. Tax authorities are required to justify their position. Most often, refusal is associated with the provision of an incomplete list of documents. In this case, the situation must be corrected within one month from the date of receipt of the notification. However, you do not need to reapply for a tuition deduction.

If the problem is not related to the documents, you need to eliminate the discrepancy with the requirements for processing deductions and resubmit the application for consideration. Under certain circumstances, you may not be able to get some of your money back. For example, if the statute of limitations has passed.

Results and conclusions

From now on, it is clear which documents for tax deduction for education are provided in a given case. As already mentioned, all listed papers are attached along with copies certified by a notary. Only then can we speak with confidence about the authenticity of the papers.

In fact, getting your tuition money back is not that difficult. It is recommended to contact the tax authorities annually. Some people prefer to claim a deduction for 3 years of study at once. This is also possible. You can submit an application for consideration at any time from the moment the right to deduction arises.

How long does it take to complete the transaction? Typically, receiving a deduction takes 3-4 months. At the same time, most of the time you have to wait for a response from the tax authorities. Document verification is carried out carefully, and therefore there is a long wait. What list of documents is needed for a tax deduction for education? It's no longer a mystery.

An application for a personal income tax refund for training will be needed if you intend to receive 13% of the expenses spent on training (your own or close relatives) from the budget. Who has the right to count on receiving social benefits? Where can I get it? What documents need to be collected? We will study the answers to these and other questions in the article below, and also consider the nuances of drawing up and a sample of filling out an application for a tax deduction.

Features of the tuition deduction

The Tax Code of the Russian Federation provides for the possibility of returning from the budget part of the expenses incurred by the taxpayer when paying for training. Such a refund occurs by reducing the tax base for personal income tax by the amount of these expenses. This reduction is one of the types of social tax deductions (Article 219 of the Tax Code of the Russian Federation) and is characterized by the following (subparagraph 2, paragraph 1 and paragraph 2, Article 219 of the Tax Code of the Russian Federation):

- It can be obtained for expenses both for your own education and for the education of your children, brother, sister or ward.

- An educational institution must have a license.

- Own training can occur at any age, in any form and is limited only by the amount of expenses allowed according to the total amount of social deduction for oneself for each year (RUB 120,000).

- When paying for the education of children, a brother, sister or ward, there are restrictions on their age (up to 24 years), form of education (full-time) and limit annual expenses for each of them (RUB 50,000).

- Actual expenses on payment documents are subject to deduction.

- If training costs are paid by maternity capital, then no deduction is provided.

- A tax refund will be possible only if the taxpayer had income taxed at a rate of 13% and paid personal income tax on it. If the amount of annual income is less than the educational expenses incurred, only the amount of tax actually paid for the year will be refunded.

Read about other social deductions .

Who will provide the deduction and when?

The deduction can be provided by both tax authorities and employers.

In the first case, the issue of deduction can be resolved only after the end of the year in which study expenses took place, when the amount of annual income and the amount of tax withheld from it is already known, but no later than 3 years from its end.

The taxpayer collects 2-NDFL certificates from all places of work for the past year and, on their basis, draws up a 3-NDFL declaration, filling it in with data on both income and all types of deductions, adding training expenses to them. By increasing the amount of deductions, the result of the declaration, calculated in section 2, will be the amount to be returned from the budget.

Attention! Valid since 2019 new form declaration 3-NDFL. You can download it.

The declaration, along with the originals of 2-NDFL certificates and a set of documents confirming deductions, is submitted to the Federal Tax Service at the place of residence. The legislation does not provide for the simultaneous submission of an application for a tax deduction for education, and the Federal Tax Service considers a declaration to be such an application. However, the taxpayer must indicate somewhere the details of the account to which he wants to receive the money returned to him (Clause 6, Article 78 of the Tax Code of the Russian Federation), so the application is still necessary. But this will not be an application for a deduction, but for a tax refund with the details of the taxpayer’s bank account.

The refund will be made by the Federal Tax Service 4 months from the date of filing the declaration after passing the following stages:

- within 3 months (clause 2 of article 88 of the Tax Code of the Russian Federation) the declaration is checked;

- the necessary actions for tax refund are carried out within a month from the date of acceptance of the declaration (clause 6 of article 78 of the Tax Code of the Russian Federation).

Since 2016, employers can also provide a tax deduction for training. To do this, the taxpayer must receive from the tax authority a document confirming the right to the deduction and present it along with the application to the employer.

Documents for tuition deduction

The set of documents giving the right to deduct educational expenses includes:

- a copy of the educational institution's license;

- a copy of the training agreement;

- copy of the passport;

- a copy of the TIN assignment certificate;

- original receipt of tuition payment.

If it was not the taxpayer himself who studied, then you will need:

- a copy of the child's birth certificate;

- copies of documents confirming the fact of relationship or guardianship;

- original certificate of full-time study.

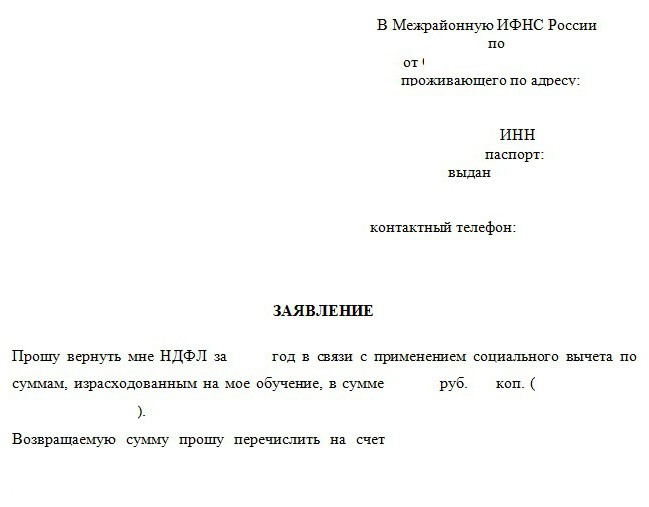

Sample application for tax deduction for education

Starting from 01/09/2019, an application for a tax refund is drawn up according to the form from Appendix 8 to the order of the Federal Tax Service of the Russian Federation dated 02/14/2017 No. ММВ-7-8/182@ as amended by the Federal Tax Service order No. ММВ-7-8/670@ dated 30/11/2018.

A tax deduction for a child’s education is one of the social tax deductions that is available to parents who are officially employed, whose child is studying in a paid full-time department of an educational institution, and has not reached the age of 24.

The Tax Code (clause 2 of Article 219) defines the procedure for providing a social tax deduction for training expenses. It says that social tax deductions for education expenses are available to citizens who pay for:

- your training in any form of education (day, evening, correspondence and any combination thereof);

- paid education for your child under the age of 24;

- paid training ward ward(s) under the age of 18 years in full-time education;

- training of former wards under the age of 24 (after the termination of guardianship or trusteeship over them) in full-time education;

- full-time education of his brother or sister under the age of 24, who are full-blooded (i.e., having a common father and mother with him) or not full-blooded (i.e., having only one common parent with him).

In 2017, according to the Federal Tax Service of Russia, in 2017 (letter No. BS-3-11/4769 dated October 14, 2016), expenses for the education of a spouse cannot be reimbursed.

Let us consider in more detail the grounds and procedure for registering and receiving a social tax deduction regarding the education of children.

Parents have the right to partially refund the personal income tax they paid on the amount paid for their child’s education in the amount of 13 percent.

What is the size of the social tax deduction for education in 2017?

The maximum possible amount spent on children's education from which it is possible to receive a social tax deduction in 2017 is 50 thousand rubles per year. This means that the maximum amount of tax that the tax authority can return for the year will be 6 thousand five hundred rubles per year for the education of each child.

But the amount from which you can receive a tax deduction for the education of the parents themselves, or their brothers and sisters, is already 120 thousand rubles per year.

Thus, deduction for education is a multiple-time process. You can apply for it every year. For each year, no more than the amount of personal income tax withheld into the budget is allowed to be returned.

Requirements for the educational institution

In order for the tax authority to positively consider an application for a social tax deduction for expenses incurred on training, it is necessary that the educational institution has a license to this type educational activities. These educational institutions include: If they have a license or other document confirming the right to conduct educational process Universities, secondary educational institutions, children's educational institutions (paid kindergartens), institutions additional education(art school, music school, sport school paid bases).

At the same time, it does not matter what type of property this educational institution belongs to. These can be both public and private educational institutions, and not only Russian ones.

An important requirement tax service is the fact that tuition receipts must be issued to the taxpayer, and not to the child or person for whom the payment is made.

How to get a tax deduction for a child's education?

A. When submitting documents to the tax authority

To exercise the right to a tax deduction for educational expenses, a parent must take the following steps step by step:

Fill tax return(according to Form 3-NDFL) at the end of the year in which tuition was paid.

Obtain a certificate from the accounting department at your place of work about the amounts of accrued and withheld taxes for the corresponding year in form 2-NDFL.

Prepare a copy of the agreement with the educational institution for the provision of educational services, which specifies the details of the license to carry out educational activities (if there are no license details in the agreement, you must provide a copy of it), and if the cost of education increases, a copy of the document confirming this increase, for example, an additional agreement to the contract indicating the cost of training.

If you paid for the education of your own or a ward child, brother or sister, copies of the following documents are additionally provided:

- a certificate confirming full-time study in the corresponding year (if this clause is not included in the agreement with the educational institution for the provision of educational services);

- child's birth certificate;

- documents confirming the fact of guardianship or trusteeship - an agreement on the implementation of guardianship or trusteeship, or an agreement on the implementation of guardianship over a minor citizen, or an agreement on a foster family (if the taxpayer spent money on the education of his ward);

- documents confirming relationship with a brother or sister (if the education of the brother or sister was paid for).

5. Prepare copies of payment documents confirming the taxpayer’s actual expenses for training (cash register receipts, cash receipt orders, payment orders, etc.).

6. Submit to the tax authority at your place of residence a completed tax return with copies of documents confirming actual expenses and the right to receive a social tax deduction for educational expenses.

If the provided tax return calculates the amount of tax to be refunded from the budget, together with the tax return, you must submit an application to the tax authority for a personal income tax refund in connection with training expenses.

The amount of overpaid tax is subject to refund upon application of the taxpayer within one month from the date the tax authority receives such an application, but not earlier than the end of the chamber tax audit(Clause 6 of Article 78 of the Tax Code).

When submitting copies of documents confirming the right to deduction to the tax authority, you must have their originals with you for verification by a tax inspector.

B. When submitting documents at the place of work

The social tax deduction can be obtained before the end of the tax period by contacting the employer, having previously confirmed this right with the tax authority. To do this, the taxpayer must:

Write an application to receive a notification from the tax authority about the right to a social deduction. A sample application can be found in Letter of the Federal Tax Service of Russia dated December 7, 2015 No. ZN-4-11/21381 “On receiving social tax deductions provided for in subparagraphs 2 and 3 of paragraph 1 of Article 219 of the Tax Code Russian Federation, from tax agents,” or ask for a sample from the accounting department at your place of work.

Prepare copies of documents confirming the right to receive social benefits.

Submit to the tax authority at your place of residence an application to receive notification of the right to a social deduction, attaching copies of documents confirming this right.

After 30 days, receive a notification from the tax authority about the right to a social deduction.

Provide a notice issued by the tax authority to the employer, which will be the basis for not withholding personal income tax from the amount of income paid to an individual until the end of the year.

A sample application for a personal income tax refund can be found on the official website of the Federal Tax Service of Russia

How to fill out a tax return in form 3-NDFL for a tax deduction for children's education?

The tax return for personal income tax in form 3-NDFL is filled out on the basis of data from the income certificate in form 2-NDFL (which is issued by the accounting department at the place of employment).

The declaration itself is quite voluminous and its form and content may change from year to year, therefore, it is not recommended to use its forms for the previous year, much less older ones. Before filling it out, you should carefully study the tax document that is current at the time of filling it out. (To do this, you need to use the current Order of the Federal Tax Service of Russia regarding the procedure for filling out the tax return form for personal income tax). It can be quite difficult to fill out this form correctly and without errors the first time.

The declaration form itself is easy to obtain on the tax authority’s website. The “Taxpayer’s Personal Account” is available there. There is a special tax service program in which all incorrect actions and errors when filling out the form are visible.

At self-filling In the form, it is important to indicate the following data and details: tax office number, full name of the taxpayer, his TIN, details of his passport, country code, information about the place of residence, code municipality, name of the organization, checkpoint, OKTMO organization according to certificate 2-NDFL), amounts by month (from the same form). On the “income” tab, you need to select “13” - this is 13% taxation. If there were vacation pay in any month, code 2012 is entered, for salary code 2000. The total amount of income must match that in the 2NDFL certificate. In the “Deductions” tab, fill in “Amounts paid for children’s education.” After the form is ready, an application is submitted indicating the calculated amount of the tax deduction refund for the child’s education.

Examples of calculating tax deductions for education

- In 2016, Yulia studied at a driving school for her license. Her expenses for such studies amounted to 55,000 rubles. At the same time, Yulia received a monthly salary of 35,000 rubles. She earned 42,000 rubles a year. Tax was withheld from her into the budget (13 percent), which amounted to 54,600 rubles.

Tax deduction calculation: 55,000 * 13% = 7,150 rubles. This is the amount that she will return as a tax deduction (and in the fullest possible amount, since more tax was withheld from her in 2016).

- Ivan is a student in the commercial (paid) department and works part-time. Therefore, his annual earnings amounted to 115,000 rubles. A tax of 14,950 rubles was withheld from this income. Personal income tax. In 2016, tuition fees cost him 125,500 rubles.

Tax deduction calculation: annual tax was withheld from Ivan in an amount significantly less than the amount maximum size deduction. He will be able to return only 14,950 rubles, that is, the amount that was paid as tax on earned income.

- Maria has three dependent children. Her income for 2016 was 45,000 rubles. per month before tax. This amounted to an annual taxable income of 540,000 rubles. The accounting department at work withheld personal income tax in the total amount of 70,200 rubles.

In the same year, Maria paid:

- 5,000 rubles - for paid kindergarten for one child;

- 37,500 rubles - for another child’s paid children’s music school;

- 68,300 rubles - for the education of the third child in an educational institution.

Tax deduction calculation: Maria will receive 6,500 rubles for kindergarten. (restricted by law). For music school - 37,500 * 13% = 4,875 rubles.

For the eldest child’s studies at an educational institution, 6,500 rubles will again be returned. In total, she is entitled to 17,875 rubles. Thus, Maria will have the maximum tax deduction in total, since the amount of tax withheld from her turned out to be greater.

In conclusion, let us remind you that there is no need to delay applying for a tax deduction, since, according to paragraph 7 of Article 78 Tax Code In the Russian Federation, the right to receive a tax deduction for the education of children is valid for only three years from the moment the funds for education were paid.

The social tax deduction allows you to reduce your income subject to personal income tax at a rate of 13% (with the exception of income from equity participation in organizations, and from 01/01/2018 also winnings in gambling and lotteries), that is, pay less tax. But at the same time, you must have the status of a tax resident (clause 3 of Article 210, clause 1 of Article 224 of the Tax Code of the Russian Federation; clause 1 of Article 1, Article 2 of the Law of November 27, 2017 N 354-FZ).

Reference. Tax residents

By general rule tax residents are recognized as individuals who are actually located in the Russian Federation for at least 183 calendar days within 12 consecutive months (clause 2 art. 207Tax Code of the Russian Federation).

1. Conditions for receiving a social deduction for training

This social tax deduction can be received by: individuals who paid (clause 2, clause 1, article 219 of the Tax Code of the Russian Federation):

Your training;

Education of your children, wards (that is, persons for whom the taxpayer is a guardian or trustee);

Teaching your brothers and sisters (including half-siblings).

When a taxpayer pays for the education of other persons, in particular his or her spouse, the taxpayer is not given a deduction. At the same time, when paying for a child’s education, taxpayer-spouses have the right to take advantage of a social tax deduction, regardless of which of them has documents confirming educational expenses. In this case, each spouse must be the parent of the child. Also, a deduction is provided in case of payment for training of a taxpayer by his representative on the basis of a power of attorney, if the payment documents contain information that allows identifying such a taxpayer (Letters of the Federal Tax Service of Russia dated October 24, 2016 N BS-4-11/20142@, dated December 22, 2016 N BS-4 -11/24757@; Letter of the Federal Tax Service of Russia for Moscow dated June 10, 2013 N 20-14/057666@).

The deduction is provided when studying in educational organizations that have the appropriate license, which can be either state or municipal, or private (for example, fee-paying schools, lyceums, sports and music schools, universities). In addition, a deduction can be obtained when studying with individual entrepreneur, attracting teaching staff and having the appropriate license. If training is carried out by an individual entrepreneur directly, in order to receive a deduction, it is necessary that the Unified State Register of Entrepreneurs indicate information about the implementation of educational activities by the individual entrepreneur. In this case, the individual entrepreneur is not required to have a license (paragraph 3, paragraph 2, paragraph 1, article 219 of the Tax Code of the Russian Federation; Letter of the Federal Tax Service of Russia dated November 18, 2015 N BS-4-11/20124@).

You can use the deduction for those years when you paid for training and such training was carried out, including the time of academic leave (paragraph 4, paragraph 2, paragraph 1, article 219 of the Tax Code of the Russian Federation).

If you paid for multi-year education at a time, you can receive a deduction only once - for the year in which the payment was made.

Moreover, if you spent a large amount, then it is impossible to transfer the unused balance to the next year (Letter of the Federal Tax Service of Russia dated August 16, 2012 N ED-4-3/13603@).

1.1. Social deduction for your education and the education of your brothers and sisters

A student is given a deduction for his or her education in any form of education (full-time, part-time, part-time, part-time) regardless of age.

You can receive a social deduction in connection with paying for the education of brothers and sisters (including half-siblings) unless at the time of payment they have reached the age of 24 years and their education is full-time (paragraph 6, paragraph 2, paragraph 1, Article 219 Tax Code of the Russian Federation).

A deduction can be received in the amount of actual expenses for training, but not more than 120,000 rubles. in a year. Moreover, this maximum amount is common for all types of social deductions (with the exception of deductions in the amount of expenses for the education of children and for expensive treatment). Therefore, if you use social deductions for several types of expenses, then they overall size will be limited to 120,000 rubles. (paragraph 7, clause 2, article 219 of the Tax Code of the Russian Federation; clause 12.6 of the Procedure, approved by Order of the Federal Tax Service of Russia dated December 24, 2014 N ММВ-7-11/671@).

1.2. Social deduction for education of children and wards

The deduction is provided if you paid for full-time education (clause 2, clause 1, article 219 of the Tax Code of the Russian Federation):

Children under 24 years of age;

Wards under 18 years of age, as well as former wards under 24 years of age.

Having confirmed the fact full-time training children (wards), you can receive a social deduction even if they receive education remotely (Letter of the Ministry of Finance of Russia dated September 25, 2017 N 03-04-07/61763).

The deduction is not provided if you paid for the education of other persons (grandchildren, nephews, etc.).

The amount of deduction is limited to RUB 50,000. per year per student. Moreover, this is the total amount for the application of the deduction by two parents, guardians, and trustees (clause 2, clause 1, article 219 of the Tax Code of the Russian Federation).

Example. Deduction for education of two children

When training two children, one of the parents has the right to receive a deduction in the amount of expenses incurred, but within the limit of 100,000 rubles. per year (50,000 rubles for each child). If both parents claim a deduction, then each of them will have a limit of 50,000 rubles. in a year.

The deduction cannot be used if tuition was paid at the expense of maternity capital (paragraph 5, paragraph 2, paragraph 1, article 219 of the Tax Code of the Russian Federation).

2. The procedure for receiving a social deduction for training

You can receive a social tax deduction in two ways - from your employer and from the tax authority. Let's look at each of them in detail.

2.1. Obtaining a social tax deduction from an employer

You can receive a tax deduction before the end of the calendar year in which you paid for training by contacting your employer with a corresponding application and confirmation of the right to receive social tax deductions issued by the tax authority for a certain form(paragraph 2, paragraph 2, article 219 of the Tax Code of the Russian Federation).

Step 1: Prepare supporting documents

To confirm your right to a social deduction for training, you will need (paragraph 3, paragraph 2, paragraph 1, article 219 of the Tax Code of the Russian Federation; Letter of the Federal Tax Service of Russia dated November 22, 2012 N ED-4-3/19630@):

1) a copy of the training agreement (if concluded);

2) copies of the license educational organization, if its details are not specified in the contract;

3) copies of payment documents confirming payment for training. For example, cash receipts, receipts for receipts cash orders, paid bank receipts, etc.

If you are claiming a deduction for the education of children, wards, siblings, then you will additionally need:

1) a copy of a document confirming the relationship and age of the student - if you paid for the education of children, brothers, sisters. For example, a copy of your birth certificate;

2) a document confirming full-time study (if it is not specified in the contract). In particular, this may be a certificate from an educational institution;

3) a copy of the document confirming guardianship or trusteeship - if you paid for the education of your wards.

Additionally, you can check the list of documents with your tax office.

Step 2. Receive from the tax authoritynotificationon confirmation of the right to deduction

Supporting documents, along with an application to confirm the right to a social deduction, must be submitted to the tax office at the place of residence. Including documents can be sent via Personal Area taxpayer. There is no need to submit a declaration in Form 3-NDFL.

A notice of confirmation of the right to deduction is issued by the tax authority no later than 30 calendar days from the date of submission of the application and supporting documents to the tax authority (clause 2 of article 11.2, paragraph 2 of clause 2 of article 219 of the Tax Code of the Russian Federation).

Step 3. Submit an application and notification to the employer confirming the right to deduction

An application for a social tax deduction is drawn up in free form. Submit it to your employer along with the notice confirming your entitlement to the deduction.

Step 4. Receive a social tax deduction from your employer

The employer must provide you with a deduction starting from the month in which you contacted him with the specified documents.

If the employer withheld personal income tax without taking into account the tax deduction, he is obliged to return to you the amount of excess tax withheld. To do this, submit an application to the accounting department for the return of excessively withheld personal income tax, indicating in it the bank account for transferring the overpayment. The employer must transfer the excess withheld amount to you within three months from the date of receipt of your application for its return (clause 2 of Article 219, clause 1 of Article 231 of the Tax Code of the Russian Federation).

2.2. Obtaining a social tax deduction from the tax authority

At the end of the calendar year in which you incurred tuition costs, a social deduction may be provided tax office at your place of residence. In particular, you have the right to apply to the tax authority for the balance of the deduction if the employer was unable to provide it to you in full (paragraph 1, 5, paragraph 2, article 219 of the Tax Code of the Russian Federation).

Step 1. Fill out the tax formdeclarationAndstatementabout the return of overpaid personal income tax amounts

To contact the tax authority, you will need the same supporting documents as when applying for a notification of the right to deduction (step 1 of the previous section), as well as a certificate of income in form 2-NDFL. This should be requested from the employer.

Note. View and download certificates2-NDFLcan be done in your personal account on the website of the Federal Tax Service of Russia (clause 2 art. 230Tax Code of the Russian Federation;InformationFederal Tax Service of Russia).

Based on the specified documents, fill out a tax return. You also need to draw up an application for a refund of the overpaid amount of personal income tax that arose in connection with the recalculation of the tax base taking into account the social deduction. Indicate in it the bank account details for transferring the overpayment to you. You can submit this application along with your tax return (clauses 1, 6, article 78, clause 2, article 219 of the Tax Code of the Russian Federation; clause 1.4 of the Procedure; Letter of the Federal Tax Service of Russia dated October 26, 2012 N ED-4-3/18162 @).

Note. You can fill out the declaration using free program on the website of the Federal Tax Service of Russia.

Step 2: Submit your tax return and supporting documents to the tax authority

As a general rule, the declaration is submitted to the tax authority at your place of residence no later than April 30 of the year following the year in which you paid for training (clause 3 of Article 80, clause 1 of Article 83, clauses 1, 2 of Art. 229 of the Tax Code of the Russian Federation).

But if you submit a declaration solely for the purpose of obtaining tax deductions, you can submit it at any time within three years after the end of the year in which you paid for education (clause 7 of article 78 of the Tax Code of the Russian Federation).

The declaration can be submitted (clause 4 of article 80 of the Tax Code of the Russian Federation):

Personally or through a representative;

By post with a description of the attachment;

In electronic form, including through the Unified Government Services Portal or the taxpayer’s personal account.

Step 3. Wait for the tax authority’s decision and refund

The tax authority, within three months from the date you submit your declaration and supporting documents, conducts a desk audit, after which it will send you a notification about the decision taken, including refusal to refund overpaid tax (clause 9 of article 78, clauses 1, 2 of article 88 of the Tax Code of the Russian Federation).

If the fact of overpayment of tax is established and the right to deduct personal income tax is confirmed, the corresponding amount of overpayment is subject to refund within a month from the date of receipt of your application for a tax refund or the end of the desk audit, if you submitted the application along with the declaration (clause 6 of article 78 of the Tax Code of the Russian Federation ; Letter of the Federal Tax Service of Russia dated October 26, 2012 N ED-4-3/18162@).

"Electronic magazine "ABC of Law", current as of 12/07/2018

Find other materials from the ABC of Law magazine in the ConsultantPlus system.

The most popular ABC of Law materials are available in.