See pages where the term capitalization level is mentioned. Market capitalization is a simple way to assess the value of a company

Read also

Let's consider capitalization rate. It is included in the group of indicators of the financial stability of an enterprise and characterizes long-term solvency. The capitalization ratio belongs to the group of financial leverage ratios; this group includes indicators characterizing the ratio of own and borrowed money. In Western sources, the capitalization ratio is referred to as Capitalization Ratio.

I will consider the capitalization ratio according to our usual analysis scheme. First, we will reveal the economic essence of the coefficient, then we will give a calculation formula, and calculate the coefficient for domestic company and in conclusion let us remember optimal values indicator.

Capitalization rate. Economic essence

As mentioned above, capitalization ratio refers to financial leverage ratios, and they determine the efficiency of use of borrowed capital by an enterprise. It shows how our enterprise depends on borrowed funds.

How is the capitalization ratio read?

If the value of the capitalization ratio decreases, this indicates that:

- The company retains more net profit.

- The company finances its activities with its own funds.

- Investment attractiveness increases.

If the value of the capitalization ratio increases, then this tells us that:

- The risk of business activity increases.

- The enterprise increases the share of borrowed funds involved in financing its activities.

- Investment attractiveness is decreasing.

Who uses the capitalization rate?

This coefficient is extremely important for investors who analyze it to evaluate investments in a particular company. A company with large coefficient capitalization. This is explained by the fact that it will have more equity in its capital structure. However, too great importance the coefficient is not very good for the investor, since the profitability of the enterprise and thereby the income of the investor decreases.

This coefficient is also used creditors. The situation with them is exactly the opposite for investors. The lower the capitalization ratio, the more preferable it is to provide a loan.

What are the synonyms for capitalization ratio?

Capitalization ratio has the following synonyms:

- Financial leverage ratio,

- Financial risk coefficient,

- Attraction rate,

- Leverage of financial leverage,

- Debt to equity ratio,

- Self-financing ratio.

In fact, all the names listed above are one capitalization ratio, but often in different literature it is called differently. Therefore, it is useful to know its similar names.

Capitalization rate. Calculation formula

Capitalization rate formula has the following form:

Capitalization ratio = Liabilities/Equity =

(Long-term liabilities + Current liabilities)/Equity=

(p.1400+p.1500)/p.1300

All data for calculation can be taken from the “Balance” form. It is important to note that under “Liabilities” in the formula, various authors use either the sum of short-term and long-term liabilities or only long-term liabilities. Thus, the following formula also holds:

Capitalization ratio = Long-term liabilities/Equity = line 1400/line 1300

Until 2011, the formula for calculating the capitalization ratio was as follows:

Capitalization ratio = (line 590+line 690)/line 490

In foreign literature you can find the following formula for calculating the coefficient:

Capitalization rate. Calculation using the example of OJSC MMK

Capitalization ratio for OJSC MMK

For calculations we need a public financial statements, which can be obtained from the SPARK or InvestFunds service. Our example took four quarters of 2013 and the first three quarters of 2014.

As you can see, we only work with lines from the “Passive” section. Capitalization ratio for OJSC MMK:

Capitalization ratio 2013-4 = (50199274+78705285)/138414101 = 0.9

Capitalization ratio 2014-1 = (48096120+90037849)/137873396 = 1

Capitalization ratio 2014-2 = (45956368+87681300)/147094603 = 0.9

Capitalization rate 2014-3 = (37257076+100154968)/150436511 = 0,91

As you can see, during the year of calculations the coefficient almost did not change and was at the level of 1. This is a standard value for domestic enterprises. We can conclude that OJSC MMK has a share of borrowed funds equal to the share of its own funds (50/50%). Below we will talk in more detail about standard values.

Capitalization rate. Normative value

Let's talk about standard values. In the domestic literature, the capitalization ratio is considered optimal for an enterprise when value 1. In other words, the company has equal shares of borrowed and equity capital (50% borrowed capital, 50% equity).

In economically developed countries, the coefficient is 1.5 (60% borrowed capital, 40% equity)

The standard for the coefficient depends on the industry of the enterprise, the size of the enterprise, capital intensity of production, period of existence, profitability of production, etc. Therefore, the ratio should be compared with similar enterprises in the industry. This will provide a clearer picture of the finances of the enterprise.

Summary

So, we have looked at one of the most important ratios for investors and lenders - the capitalization ratio. The higher its value for an enterprise, the more preferable it is for investors and less for creditors. A high value of the ratio indicates that the company is losing financial stability; too low a value - the company loses profitability. The capitalization indicator must be used in conjunction with the profitability and liquidity ratios of the enterprise. Read more about the main profitability indicator in the article: ““.

Thank you for your attention!

Today we will dwell in detail on such a concept as “capitalization”. In economic literature, this term usually means the use of a company’s free capital to increase income.

Thanks to capitalization, the enterprise not only increases the amount of available capital, but also other material assets. The capitalization process is best viewed at specific example. Let's say you put a hundred dollars into production and received an income of $50. The capitalization process involves investing the $50 received in the form of profit into production in order to expect to receive even more income.

Capitalization. Peculiarities

The increase in capital during capitalization depends on various factors, including special attention deserve:

- The amount of income of the company. The higher the organization's profit, the greater the amount of additional capital. If all additional capital is used to increase the company's assets, then the volume of material assets will increase, which will allow the company to effectively develop and enter new market segments.

- Liquidity of shares/bonds of the enterprise. This factor significantly influences capital increases.

To determine the percentage of capitalization of a particular enterprise, its financial condition should be assessed at least once a year. You can also use reporting for 2-3 years, which makes it possible to identify a trend towards an increase/decrease in this indicator.

To determine the percentage of capitalization of a particular enterprise, its financial condition should be assessed at least once a year. You can also use reporting for 2-3 years, which makes it possible to identify a trend towards an increase/decrease in this indicator.

In the credit and financial sector, the term “capitalization” usually means the addition of profit received in the form of interest to the body of the deposit.

The term "capitalization" is also used in stock markets. In this case, this concept has no connection with financial/current assets. In the stock market, to determine the percentage of capitalization, the increase in the volume of shares/bonds that are in circulation is taken into account.

Market capitalization

The concept of “market capitalization” means the percentage increase in capital of both the organization being valued and a specific market segment. When identifying a company's capital increase, it is best to look at a specific example.

It is necessary to refer to the available reports for several years, which will allow us to clearly see the growth/decrease in the volume of available capital. If we have identified a sharp increase this characteristic, we can conclude that the enterprise is developing successfully.

Key Feature is that when calculating capital gains, not only the company’s own money, but also the company’s credit money is taken into account. Because of this feature, the actual state of the enterprise may definitely not be correct.

Key Feature is that when calculating capital gains, not only the company’s own money, but also the company’s credit money is taken into account. Because of this feature, the actual state of the enterprise may definitely not be correct.

To avoid such a development, experts in the financial industry identify capital increases based on price valuable papers of the enterprise in question. This is because the price of a firm's shares/bonds provides a specific measure of the company's net income.

It is customary to distinguish several main types of market capitalization, including:

Main forms of capitalization

Modern economic literature distinguishes several forms of capitalization, depending on the means by which Money capital is being built up. In accordance with this classification, capitalization can be of the following types:

- Market.

- Real.

- Marketing.

Real capitalization reflects the effectiveness of the company's current economic policy. To calculate it, the growth/decrease in the company's liabilities and assets is taken into account.

Market capitalization is calculated by assessing the growth/decrease in the value of a company's shares/bonds on the stock market.

Marketing capitalization does not display current state enterprises, since with this type of capitalization an increase in the volume working capital happens only on paper. Marketing capitalization, in essence, is a ploy that allows you to sell a company for much more than its real value. I hope this material helped all novice investors understand what capitalization is.

M.V. Dedkova JSCB "Settlement United Union European Bank"

Scientific publication of the Federal State Educational Institution of Higher Professional Education RGUTiS, magazine "Bulletin of MGUS" Issue "Economics", No. 1 for 2007

Capitalization is one of the few economic phenomena in which extremely high interest is shown in practice and which, until recently, has been extremely insufficiently studied in the domestic economic literature. Independent research in the field of capitalization appeared only in last years. These include dissertations by Permyakov A.S. on the topic “Investment support and capitalization management of oil and gas companies”, Ovsyannikova A.N. on the topic “Capitalization of industrial enterprises in Russia as a factor in increasing their economic sustainability”, Ezhova Yu.V. on the topic “Method of capitalization of the sinking fund machine-building enterprise", Kazintseva V.V. on the topic “Market capitalization of Russian industrial corporations as a factor in increasing the economic efficiency of production”, Ovsepyan D.E. on the topic “Management of capitalization of industrial corporations”, Pivenya V.V. on the topic “Modeling the influence economic factors on the market capitalization of industrial corporations,” Galtseva E.V. on the topic “Capitalization as a factor in strengthening the financial stability of service sector enterprises”, Varoko A.Sh. on the topic “Managing the capitalization of investment resources of the reproductive potential of the region’s agro-industrial complex.”

Thus, the list of independent studies in the field of capitalization is so small that it can be presented almost in full. In most of the above studies, capitalization is considered from the perspective of increasing the company's equity capital. In this case, the emphasis is mainly on joint stock companies, whose shares are in free circulation. In this case, capitalization is assessed based on the market value of the shares. This is the most common approach to capitalization in the domestic market, borrowed from foreign practice. Because of this, it has a very limited scope of application in the domestic economic environment, where the joint-stock form of capital has not yet become widespread. Consequently, with this approach to capitalization, most Russian companies fall out of the object of study.

Only in the study by Galtseva E.V. an attempt has been made to show various shapes manifestations of capitalization on the Russian market. Depending on the mechanism for increasing capitalization, the author identifies three forms:

- real capitalization;

- marketing or subjective capitalization;

- market or fictitious capitalization.

All of the above forms of capitalization are reflected in the companies’ balance sheets in the form of increasing their own sources of financing (Section 3 of the balance sheet), but have various sources origin and various ways initiation.

Real capitalization

An efficiently operating enterprise almost always has a positive financial result. economic activity. Profit, or rather its reinvested part, accumulates in section 3 of the balance sheet, largely determines the value of the enterprise and leads to an increase in equity capital. High capitalization indicates the ability of a business entity to generate income, effectively use resources, and expand its business, which, in turn, is a condition for future profitability.

Meanwhile, an increase in section 3 of the balance sheet, other things being equal, means an increase in liabilities and, therefore, due to the basic rule of balance sheet management, causes an increase in the assets of a business entity. Depending on the type of activity, the strategy of the enterprise and the existing current problems, the increase affects either non-current or current assets, or both at the same time. If, as a result of financial and economic activities, an enterprise reinvests profit, directing it to replenish non-current assets (primarily means of labor) and current assets (in terms of labor items or inventories), real capitalization occurs, expressed in an increase in the real value of property. In most cases, companies with a strong strategy invest their capital gains in long-term assets, i.e. in section 1 - non-current assets.

In this case, capitalization is a natural result of financial and economic activity, is economically objective and is initiated by sources of financing, i.e. balance sheet liabilities. Real capitalization leads to strengthening the financial stability of the company, increasing its credit rating, increasing marketing attractiveness and increasing its market value.

Marketing or subjective capitalization

In practice, the process of accumulation at the on-farm level is often the result of active marketing policy And advertising campaign, which “inflate” the market value of an enterprise, separating it from its real value. In this case, the increase in the balance sheet currency, all other things being equal, occurs initially on the part of assets, as a rule, the intangible component of the balance sheet, for example, due to the following operations:

- reflection in the balance sheet of the valuation of business reputation (goodwill);

- increase in market value trademark, brand;

- reflections in accounting and, accordingly, in the balance sheet of know-how;

- acquisition of rights to the results of intellectual activity.

An increase in the property of an enterprise in this case, other things being equal, can be reflected in the balance sheet in different ways:

- balance in liabilities by the growth of additional capital;

- treat on financial results, increasing retained earnings;

- increase the authorized capital with appropriate registration in the prescribed manner.

Additional capital, retained earnings and authorized capital, in turn, increase the “equity capital” aggregate. In this case, capitalization is initiated by intra-company management on the part of assets, primarily intangible ones. Cost estimates in this case are often contractual and therefore subjective. Increase in property due to negotiated valuations, even at the cost of re-registration authorized capital is a largely subjective operation. Transactions of this kind make it possible to form a “representative” balance sheet of the company, however, given that intangible assets are high-risk assets, such capitalization may disappear with the slightest change in the political situation or market conditions. An increase in equity capital through the expansion of the authorized capital gives operations of this kind a certain stability and legal registration, however, it represents an extensive path of development of the enterprise and does not indicate the effectiveness of using its potential. This type of capitalization is called subjective or marketing capitalization, since its nature is subjective, and this form of capitalization is used, as a rule, for marketing purposes.

Subjective (marketing) capitalization has recently become very popular among PR agencies, which proceed from the fact that business reputation plays a key role in shaping the company's value. This approach to capitalization led to the emergence of the “Reputation Capitalization” project, initiated by the Publicity PR Agency. IN expert survey conducted by this PR agency, 1072 respondents from among top managers, heads and employees of marketing, advertising and PR departments, financial analysts and other experts took part large companies, more than 60% of respondents answered that business reputation is a real asset that creates value.

In the development of subjective (marketing) capitalization in Russia, property taxation previously acted as a limiting factor. True, the “containment” was insignificant, given the low property tax rate. Currently, only fixed assets reflected in the balance sheet at their residual value are taxed. This means that almost any enterprise can increase capitalization with small means and form a “representative” balance sheet, which, in turn, will lead to the activation of the subjective (marketing) form of capitalization in the Russian market.

Market or fictitious capitalization.

At the developed stages of a market economy, where the joint-stock form of ownership, free circulation of shares and determination of the market value of an enterprise through stock quotes are widespread, the understanding of capitalization as interpreted by Richard Koch is more acceptable. R. Koch believes that capitalization is “the market value of a company whose shares are listed on the stock exchange,” which is the product of the market price of the share and total number company shares. The increase in the market value of shares and the joint-stock company as a whole is reflected in this case in the balance sheet asset in the form of revaluation financial investments" and is balanced in liabilities with additional capital.

This form of manifestation of capitalization has obvious resemblance with subjective (marketing) capitalization. However, capitalization in this case is initiated not by intra-company management, but by external exchange structures that carry out stock quotes. The results of exchange trading, as is known, are influenced by a combination of objective and subjective factors, but the effect of subjective factors is minimized by public recognition.

In academic publications, capital represented in income-generating securities is called fictitious or equity capital. Since this form of capitalization is formed as a result of stock transactions, it is called fictitious capitalization. Analysts stock market prefer to call this form of manifestation of capitalization market capitalization.

In Russia, fictitious or market capitalization has recently been developing, due to the activation of the stock market. However, it is typical only for large Russian businesses formed on a joint-stock form of ownership. For most domestic enterprises, this tool for increasing their own capital, therefore, this form of capitalization is not yet available.

Along with the listed forms of manifestation of capitalization, one can distinguish such concepts as “capitalization of property” and “capitalization of expenses.”

Capitalization of property is manifested in the absolute and relative increase in property of a capital nature - non-current assets, which represent the most attractive collateral in any financial transactions and the most significant component of the company's real property. The most promising and manageable part of non-current assets are intangible assets. These include marketing strategy, client base, market monitoring methodology and results marketing research, know-how, the presence of a high reputation and qualified personnel, long-term relationships with customers and much more. Valuation of intangible assets and their reflection in accounting is an acceptable tool for property capitalization.

Capitalization of expenses means transferring part of current expenses into capital expenses. A classic example of capitalization of expenses would be advertising expenses, which are considered operating expenses, but as a result of such expenses a brand is created that can be valued in the billions of dollars. By general recognition in the business community, a brand represents intangible asset and one of the most important competitive advantages companies. However, its valuations and trends in their changes over time do not fit into the traditional rules for reflecting intangible assets in accounting. Thus, intangible assets are depreciable, i.e. transfer of their cost to the cost of the newly created product/service is carried out in parts by calculating depreciation. Upon expiration of the period of use of an intangible asset, its value is nullified. A brand can not only not lose its value over time, but also increase it. Representing an intangible asset according to all the previously listed characteristics, a brand needs a special procedure for evaluation and revaluation. Only in this case will it be possible to capitalize expenses, as a result of which it will be possible to increase the value of non-current assets by reflecting the brand in their composition.

It should also be noted that to date, the instruments of capitalization in various types activities. The most studied in this regard is capitalization in industry. Meanwhile, in the conditions of a service society, capitalization in various sectors of the service sector needs additional research.

Study practical experience capitalization, its comprehensive analysis and theoretical generalizations are important for all market participants: for enterprises that form their own image in the market, for their partners, for shareholders.

Literature

1. Galtseva E.V. Capitalization as a factor in strengthening the financial stability of service sector enterprises: Dis. Ph.D. economist, science M., 2005. 137 p.

2. Koch R. Management and finance from A to Z. St. Petersburg: Peter, 1999. 496 pp.

3. Soviet encyclopedic Dictionary. 3rd ed. M.: Soviet Encyclopedia, 1984. 1600 p.

4. Economic encyclopedia. Political Economy. M.: Soviet Encyclopedia, 1975. T. 4. 672 p.

The implication is that for investors there is no distinction between a firm's payment of dividends and its accumulation of retained earnings. If investment projects promise a level of profitability that exceeds the required level, investors may prefer the accumulation option. If the expected return on an investment is equal to the required return, then, from the investor's point of view, neither option is superior. On the contrary, if the expected profit from an investment project did not provide the required level of profitability, investors would prefer to pay dividends. Presumably, if a company can receive a profit as a result of implementing investment projects that exceeds the market capitalization level, then investors are ready to provide the company with the opportunity to spend on investment purposes as much as is necessary to finance all projects. In the second of the cases considered, the required profit is insensitive to changes in the dividend yield. Maybe dividends are more than just a means of distributing free funds

The difficulty of reorganization lies in changing the capital structure of the company in order to reduce the volume of payments with a fixed payment period. The task of formulating a reorganization plan is solved in 3 stages. At the first stage, it is necessary to conduct a general assessment of the value of the reorganized company. Apparently, this stage is the most important and at the same time the most difficult. Trustees, who are usually responsible for its implementation, usually use the income capitalization method when assessing. If the reorganized company's projected revenue is $2 million, and the average capitalization level for similar companies is 1096, then the total value of the company will be estimated at $20 million. However, due to the difficulties of calculating a company's projected earnings and determining an acceptable level of capitalization, this estimate is subject to significant fluctuations. Thus, the value obtained as a result of the valuation is nothing more than a forecast of the potential value of the company. Despite the fact that capitalization of income is a generally accepted method of valuing a company during its reorganization, if the liquidation value of the company's assets is large enough, this valuation may be changed upward. Of course, the company's shareholders would want this valuation to be as large as possible, and in the event that the value proposed by the trustee is inferior to the liquidation value of the company, liquidation will be more in their interests than reorganization.

Part 4 introduces the cost approach to common stock selection. Based on data on dividends, growth rates, assets and ability to make a profit, the level of capitalization and an assessment of the company's intrinsic value are calculated. Options, warrants and convertible bonds are considered.

Relative value assessment. The third approach focuses not on intrinsic value but on relative value. In this approach, analysts do not accept the idea that intrinsic value is completely independent of the current stock price level, but instead seek to determine the relative value of a stock in terms of the existing market price level. For example, you can set the capitalization level for a particular issue relative to the capitalization level of the earnings or dividends of some selected group of stocks such as the S P 500 relative to the current capitalization level for a group of industry stocks or a comparable group of growth stocks to which the stock being valued can be classified.

In part (b) of the table. Table 3.3 presents data on the average operating costs of dealers in the over-the-counter market. They include all three types of costs: broker commissions, price differences and price effects. The figures presented refer to the total costs of conducting a two-way transaction - a purchase following a sale. The table shows that for any sector the size of the package is directly related to the amount of transaction costs. It can also be noted that for any fixed package, the higher the level of capitalization, the lower the percentage of costs for the operation. (A similar conclusion can be drawn by analyzing the data in part (a) of this table.)

XX century the relative level of capitalization was noticeably higher than in the 60-80s.

In general, it can be noted that the Russian banking system needs to consolidate existing credit institutions, since more high level capitalization will allow them to provide services in volumes adequate to the needs of business entities, to compete with foreign banks and others. One of the ways to solve this problem could be

If an enterprise, when implementing an investment project, can receive a profit exceeding the market capitalization level, then the shareholders are ready to provide for investment purposes as much net profit as is necessary to finance all projects of the same level. The size of dividends in this case is determined by the residual method after covering all investment costs.

From its data it follows that a significant part of the resources saved in the economy is not used for the purpose of accumulating fixed capital. The use of saved funds for investment purposes is systematically reduced. If in 1990 92.5% of all savings were used for investment in fixed capital, then in 1999 only 63.0%, i.e. over the past nine years this share has decreased by one third. Compared to similar indicators in developed countries, this is very low level capitalization of savings (for example, in the USA this figure in 1990-1999 exceeded 108%). Gross fixed capital formation relative to its threshold reached a particularly low value in 1997-1999. In the next two years, the situation improved somewhat due to an increase in the volume of investments in fixed assets, but continues to remain alarming, requiring the attention of federal executive authorities. Understanding the objective need for a large-scale renewal of the production potential of the Russian national economy, and

By its economic nature, the rate of return for the investor and internal norm according to the project are identical, i.e. they characterize the level of capitalization of income for billing period. But in the first case, we bring the rate of income from the outside, justifying its level based on our understanding of the acceptable level of income on capital. In the second option, the rate of return is formed on the basis of objectively developing proportions of results and costs, i.e., based on the internal properties of the project and the degree of its progressiveness. In this expression, the internal rate of return characterizes the guaranteed level of capitalization of income inherent in the project.

I note that there is no such unusual interest in any country with a corporately organized business. This, one might say, is an exceptional feature of Russian business. It seems to me that this feature seriously makes it difficult to increase the investment attractiveness of Russian companies. True, recently this hidden desire to reduce the value of one’s own company, which not so long ago was inherent in its top managers, is gradually giving way to the desire to increase the level of capitalization of the company.

The influence of the largest industrial companies is also increasing. In 1995, the global economic growth rate was 2.4%, while 500 largest corporations worldwide increased sales by 11° and profits by 15°. The General Eletri company in 1996 had a capitalization level (market value of shares) of 150.26 billion dollars, in 1997 - 222.75 billion dollars. In 1996 the largest Russian companies, such as Gazprom and Lukoil, entered the world quotations. Their capitalization level in 1997 was, respectively, 12.609 billion dollars. and 6.897 billion dollars. Today in Russia the level of capitalization is very low, since there are few large companies and the valuations of their shares are undervalued. Thus, in the USA, 6,000 issuers list their shares on the stock exchange

Capitalization rate - discount rate used to determine the value of expected cash flows.

In his original approach Modigliani and Miller (MM) argue that the relationship between leverage and cost of capital is explained by the net operating income theory. They largely refuted the traditional point of view, finding a behavioral explanation for the fact that the overall level of capitalization of the firm, k0, remains unchanged at all levels of leverage.

The influence of the largest industrial companies is also increasing. In 1995, with the global economy growing at 2.4%, the world's 500 largest corporations increased sales by 11% and profits by 15%. The Oepega Ele ln company in 1996 had a capitalization level (market value of shares) of $150.26 billion, in 1997 - $222.75 billion. In 1996, the largest Russian companies, such as Gazprom and Lukoil, entered the quotation of world companies . Their level of capitalization in 1997 amounted to $12.609 billion and $6.897 billion, respectively. Today in Russia the level of capitalization is very low, since there are few large companies and the level of valuation of their shares is underestimated. For example, in the USA, 6,000 issuers list their shares on the stock exchange, in Japan - 3,000, in Germany - 650, in Russia - 200-300.

Another problem, especially worse during the highest active tees, is big expense time to process applications with this mechanism compared to an automated application selection system. The user of the automated application selection system only needs to enter an application from the terminal and then receive confirmation of its completion. A member of the Hong Kong Stock Exchange, after submitting an application, needs to wait for someone to respond to it, then agree on the quantity, and if he is a seller, then send information about the concluded transaction. Most stock exchanges in Asia, including those in Malaysia and Singapore, have significantly increased their trading volumes by introducing automated trading systems. The Taiwan Stock Exchange, with its fully automated trading system, has a daily trading volume similar to that of the Tokyo Stock Exchange (although the latter has a market capitalization level that is approximately 30 times higher). But despite this it is possible

Banks whose capitalization level is below $200 million actually lose about half of their market potential clients. However, it is possible to obtain special permits for the provision of custodial services, in which the requirement for a minimum established amount of capital becomes optional. The applicant bank must provide a fairly wide range of services in the country where it intends to engage in custodial activities. In particular, the bank must have agreements with many registrars, according to which the bank is responsible for the client's securities. In Russia, so far only Charles Manhattan Bank has received the appropriate certificate. He is also licensed

Market capitalization— an evaluative indicator that allows you to analyze the general attitude of investors towards a particular company. Although it is indicated side by side on the official websites of companies next to such parameters as EBITDA or P/E, it is difficult to call it a multiplier due to bias. It's more of a baseline for calculating more precise multiples, such as net debt. Read on to learn how to calculate the market capitalization of a company and the disadvantages of the indicator.

Market capitalization: what it is and how the indicator can be useful to an investor

Market capitalization reflects the total value of outstanding shares held by investors and owners of a company. The indicator is used to superficially assess the value of a company and analyze its dynamics over a certain period of time.

There is an overall market capitalization and exchange valuation of the common shares outstanding. Many sources interpret market capitalization as the market price per share times the number of shares outstanding, but it is an even less accurate measure for valuing a company. The correct adjustment would be for so-called capital dilution, which may include:

- options to purchase shares;

- preference shares;

- convertible bonds.

Financial statements will indicate the presence of such securities in the company’s capital, but it will be difficult to find information about them on the official website without experience. Therefore, I recommend following the optimal formula:

Market capitalization = number of common shares * current market price + number of preferred shares * current market price

All information for calculations is freely available.

Benefits of Market Capitalization for Investors

- to assess the dynamics of capitalization growth over different periods of time, on the basis of which an investment decision can be made;

- to analyze how stock prices and capitalization react to certain fundamental factors. How sensitive is the company's value to force majeure or, conversely, to positive market signals. The greater the sensitivity, the greater the risk, but the more you can make from volatility.

In my opinion, it is not advisable to compare the capitalization of companies in the same industry, as well as the value of an individual share. For example, the dynamics of Gazprom shares, despite its capitalization of almost 3 trillion rubles, is not the most attractive for investors, and the cost of shares of VTB Bank is calculated in kopecks and therefore cannot be compared, for example, with shares of Sberbank.

Derivative multiples based on capitalization: PE Ratio, PS Ratio, Price Book Ratio.

Disadvantages of valuing a company by market capitalization value

- the presence of a speculative component in the price of shares. For example, traditionally before the payment of dividends there is an increase in stock prices, and after the payments there is a rollback. The financial condition of the company remains unchanged, capitalization changes;

- ignoring other influential economic factors in the indicator. Investors who know how to analyze financial statements compare the market value of shares with the debt load and liquid assets of the company. But there are investors who invest money based on good price dynamics and someone else’s advice. It is they who unreasonably inflate the market value of securities;

- limited possibility of assessment. It is possible to make an assessment by market capitalization only of public joint-stock companies about which basic information is available.

A practical example of calculating the market capitalization of a company

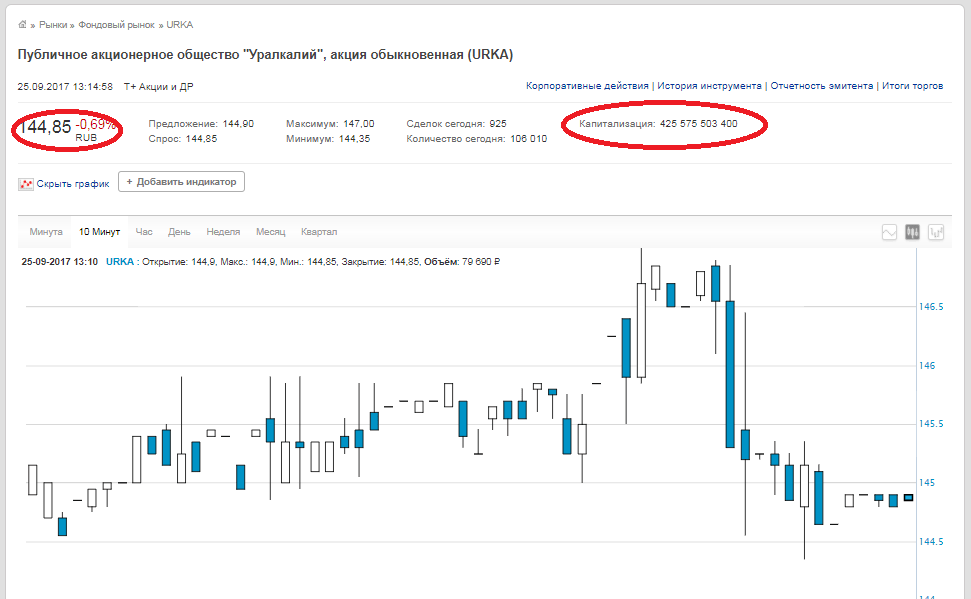

All data on the number of shares and their current value is available both on the websites of the companies themselves and analytical resources, and on the exchange itself. For example, let's take PJSC Uralkali. Number of ordinary shares - 2,936,015,891,

closing price - 144.85 rubles (data as of September 25, 2017). We multiply these numbers together and get a market value of 425.575 billion rubles. The same figure is on the exchange website.

Please note that on the exchange website in the line “Capitalization” it is not the capitalization of the company that is indicated, but the capitalization of the share, that is, if a company has ordinary shares and preferred shares, then to obtain the company’s market capitalization it is necessary to add these two numbers.

Conclusion. Calculating market capitalization versus calculating EBITDA, P/E or net debt multiples is very simple and straightforward. But it serves only as a general indicator and has large errors. I would not recommend relying solely on the dynamics of stock prices at the time of making an investment decision. You need to analyze all indicators and multipliers as a whole.

Market capitalization is used in calculating many other useful and necessary multipliers, which I will write about a little later.