Statement of changes in capital: sample completion. Instructions: preparing a report on changes in capital Report on changes in capital Word

Read also

Financial statements– this is a whole package of documents reflecting the financial activities of the company. It also includes a statement of changes in capital - this is a kind of explanatory document given to the balance sheet.

Who should write the report?

Completing a statement of changes in capital is the responsibility of all companies classified as medium and large businesses. Small businesses are exempt from the need to register it, just like organizations working in the public sector, as well as in the field of insurance and lending.

FILES

When and where to submit a document

The statement of changes in capital is of a regular nature, and the date of its preparation is the last day (according to the calendar) in the reporting period. It must be submitted to local territorial tax authorities and statistical authorities (since 2013, this obligation has been prescribed by law) within 90 days (according to the calendar) from the beginning of the new year.

Report writing rules

This report has a unified standard form recommended for use. The form can be expanded and supplemented based on the needs of the enterprise. The document contains:

- Company details,

- detailed information on the movement of three types of capital:

- additional,

- reserve,

- statutory,

- data on the share of the company's own shares,

- adjustments caused by changes in the company's accounting policies,

- information on changes in the amount of retained income and uncovered losses of the organization, etc.

Also, the report must be signed by the head of the company indicating the date of its preparation.

When filling out the form, special attention should be paid to the following points: information on changes in capital must be entered both for the last reporting period and for the two previous ones.

In addition, when drawing up a report, we must not forget that subtracted or negative values are entered in parentheses, and the units of measurement can be either millions or thousands of rubles.

Today, a report can be created and submitted to the Federal Tax Service in electronic or paper form.

You cannot make mistakes in this document, so after filling it out you need to check it very carefully and, if some inaccuracy or oversight does occur, it is better to fill out a new form.

Example of filling out a statement of changes in capital

We draw up the “header” of the document

First, the report indicates the year for which it was compiled (i.e. reporting period). Next, enter the full name of company and the following data:

- date of registration,

- OKPO code (All-Russian Classifier of Enterprises and Organizations),

- type of economic activity (required in the form of an OKVED code and decoding).

Below is entered organizational and legal status And type of ownership, and next to it are codes OKOPF(All-Russian Classifier of Organizational and Legal Forms) and OKFS(All-Russian classifier of forms of ownership). The last line of the document header contains codes OKEY(All-Russian classifier of units of measurement): i.e. thousands or millions of rubles used in the report.

Completing Section 1 of the Statement of Changes in Capital

The first part includes information:

- on the movement of three types of capital of the company: additional, reserve and authorized,

- information about shares owned by the company and acquired from holders,

- as well as income (undistributed) and losses (uncovered).

If the organization has existed for a long time, then data must be entered for the previous three years, but if the company was opened recently, then only for the last reporting period.

Under the code values in the lines are written the reasons that contributed to the change in capital, and in columns 3 to 8 - its articles.

Line 3100 shows the balance of the accounting accounts. accounting from 80 to 84 (inclusive). Data from three years ago is recorded here.

Further, in lines 3200 to 3240, information for the previous year is shown in the same way. After this, the necessary information is entered into line 3210 (below is the distribution of all financial and economic actions that led to an increase in capital in the previous year).

Column 3 shows an increase authorized capital, in particular, cells 3210 are the full size of the increase, and cells from 3211 to 3216 reflect the channels through which it occurred (in accordance with 80 accounting).

Column 4 demonstrates the price of acquired shares for joint stock companies or - for limited liability companies - parts in the authorized capital of the enterprise

Column 5- information about multiplication additional capital(source: 83 accounting account).,

A column 6- data about reserve capital(from accounting account 82).

IN column 7 information about increase in profit or loss, compiled from net profit (loss) that remained after transferring taxes and creating reserve capital (based on the values of the 84th accounting account).

Column 8 summarizes the data for all lines in the section in question.

- Line 3220 shows the values for the reduction of capital for all indicators of economic activity.

- Lines from 3221 to 3227 broadcast debit turnover according to accounting. accounts 80-84 (inclusive) and are filled in completely identical to the ones above.

The code values of lines 3230 and 3240 show changes in financial parameters of capital two types: reserve and additional.

Line 3200 reflect the total value of the company's capital on the closing day of the year preceding the reporting period, compiled as a credit balance (according to accounting accounts 80-84 (inclusive)).

Then the data for the reporting year is recorded and, in the same way as for the previous year, lines from 3310 to 3340 are filled in. Information about the increase and decrease of capital is given here, the final annual value of capital is entered in line 3300.

Completing Section 2 of the Statement of Changes in Capital

The second part of the report shows corrected values and adjustments for the amounts of profits, losses and other indicators resulting from changes in accounting policies.

Thus, if there were no changes in this part in the company’s work, and no errors were identified in previous periods of the report, then this section can be left blank.

If they were, then briefly about how to fill them out:

- V third column enter the total cost of capital of the organization as of the end of the three-year period;

- line 3400 fixes the amount compiled before the changes,

- line 3500- already corrected values;

- Below are lines detailing all the changes that have occurred.

Completing Section 3 of the Statement of Changes in Capital

The third and final section contains financial parameters of net assets as of the end of the company’s previous reporting periods.

If there are any ambiguities, separate notes are given at the end of the page.

The third form of financial statements of enterprises is a statement of changes in capital. In this article we will figure out how to fill out this form. You can download the current 2015 report form on changes in capital and a sample of how to fill it out at the end of the article for free in xls format.

Form 3 report must be submitted by all organizations at the end of the year; for 2014, the report must be submitted by the end of March 2015.

Two copies are filled out, one is submitted to the Federal Tax Service, the other to the State Statistics Committee.

Based on the title of this report, you can understand that it reflects information about changes in the organization’s equity capital, which includes authorized, additional, reserve, own shares purchased from shareholders, as well as retained earnings (uncovered loss).

In addition, adjustments resulting from changes in accounting policies or correction of errors are noted in a separate section.

Data in the report is entered as of December 31 of the reporting year and the two previous ones (2012 - 2014).

Accounting statements, in addition to Form 2, also include:

- Balance sheet - .

- Income statement - ;

- Cash flow statement - .

- Balance sheet of a small enterprise - .

- Small Business Financial Performance Report - .

Sample of filling out a statement of changes in capital

Filling out the “Capital Movement” section

This section is structured as follows: there are 6 columns for entering amounts, the first 5 reflect various types of capital, and the 6th column shows the total amount of capital.

The lines reflect the sources of capital flows.

3210-3200 – data for 2013.

3310-3300 – data for 2014. Let's take a closer look at filling out these lines of the capital flow statement. Data for 2013 can be entered based on completed report forms for the previous year.

Line by line filling:

3310 – total amount of capital increase. To be filled in if there was such an increase during the year. The increase in the authorized capital is reflected in column 3, data is taken from account 80 - credit turnover. Increase in additional - in column 5 - credit turnover of account 83. Increase in reserve (column 6) - credit turnover of account. 82. Increase in purchased own shares (column 4) – credit turnover account 81. Increase in retained earnings (uncovered loss) – credit turnover account 84. In column 7 – the sum of all values in line 3310.

3311 – 3316 – decoding of the amounts indicated in line 3310.

3320 - the total amount of reduction of each type of capital - is filled in similarly to line 3310, but the debit turnover of the specified accounts is taken.

3321 – 3327 – decryption of the amount from line 3320.

3330, 3340 – the change in reserve and additional capital is indicated separately.

3300 – the amount of each type of capital as of December 31, 2014 – balance on accounts 80, 81, 83, 82, 84.

Filling out the section “Adjustments due to changes in accounting policies and correction of errors”

3400 – total capital before adjustments.

3410 – adjustments due to changes in accounting policies.

The statement of changes in capital is prepared in the form approved by. The codes of indicators that are indicated in the Statement of Changes in Capital are given in Appendix No. 4 to this Order.

Basic rules for filling out the Statement of Changes in Capital

The statement of changes in capital is completed for the calendar year from January 1 to December 31.In addition, it provides data on the amount and changes in capital for the last year and the amount of capital for the year before last (clause 10 , 13 PBU 4/99).

To fill out the Report on Changes in Capital, you will need synthetic and analytical accounting data for accounts 80 “Authorized capital”, 81 “Own shares (shares)”, 82 " Reserve capital", 83 "Additional capital", 84 "Retained earnings (uncovered loss)".

If any data is missing, dashes are added to the lines of the Statement of Changes in Capital.

General requirements for completing the Statement of Changes in Capital

The statement of changes in equity consists of three sections.Section 1 is devoted to the movement of capital of the company. It should reflect data on the authorized, additional and reserve capital, as well as on own shares purchased from shareholders, and on the amount of retained earnings (uncovered loss). The data in the form is indicated not only for the reporting year, but also for the two previous years. Thus, in the report for 2016, in addition to the data of the current reporting period, information is provided for 2015 and 2014.

The indicators of the reporting year and previous years, which are indicated in the report, must be comparable. This allows you to analyze them in dynamics. If the company’s accounting policy did not change significantly in the reporting year, then the indicators for the previous year will coincide with the data of the previous report. If the accounting policy has changed, then it is impossible to rewrite data from last year’s document into a new report. It is necessary to make adjustments, and the reasons for the discrepancies in the indicators relating to the previous year should be indicated in the explanatory note.

In Sect. 2 reports provide information on adjustments that are associated with changes in accounting policies and correction of errors. Indicators are reflected both before and after adjustment.

In Sect. 3 enter data on the company’s net assets in the reporting and two previous periods.

The statement of changes in capital is signed by the head of the company and its chief accountant.

The tabular part of the report is filled out in thousands or millions of rubles (codes 384 or 385).

Movement of capital

This section is a table in which indicators characterizing the reasons for changes in capital are listed on the left line by line, and capital items are presented in columns on the right:- column 3 "Authorized capital";

- column 4 “Own shares purchased from shareholders”;

- column 5 "Additional capital";

- column 6 "Reserve capital";

- column 7 "Retained earnings (uncovered loss)";

- Column 8 "Total".

This line reflects the data from the year before last.

Let us show with an example what data needs to be shown in it.

Example

The organization reports for 2016.

In line 3100, the accountant will reflect the value of each part of capital as of December 31, 2014.

In line 3200 you need to reflect the amount of capital as of December 31 of the year preceding the reporting year.

If you are reporting for 2016, it is 2015.

Column 3 "Authorized capital"

Here show changes in the authorized capital for the reporting and previous years.If the company’s capital increased or decreased, then indicate the sources of the increase (reasons for the decrease) in the line-by-line transcripts.

Take the data for filling out this column from the accounting registers for account 80 “Authorized capital”.

Having shown the amount of the authorized capital, in the following lines “Increase in capital” reflect the amount of its increase.

Decipher the sources through which the authorized capital increased.

For this purpose, the report contains the following lines:

- "Additional issue of shares";

- "Increase in the par value of shares";

If during the last year the authorized capital decreased, then reflect the amount of the decrease in the lines “Decrease in capital”.

At the same time, it is necessary to disclose why such a decrease occurred.

For this purpose, the report contains the following lines:

- "Reduction in the par value of shares";

- "Reducing the number of shares";

- "Reorganization of a legal entity."

On line 3200, indicate the credit balance of account 80 at the end of last year.

Reflect the growth of the authorized capital in the reporting year in the same order as for the previous year.

- 3314 "Additional issue of shares";

- 3315 "Increase in the par value of shares";

- 3316 "Reorganization of a legal entity."

If during the reporting year the company’s authorized capital has decreased, fill in the lines in the “Decrease in Capital” section with the explanation:

- 3324 "Reduction in the par value of shares";

- 3325 "Reduction in the number of shares";

- 3326 "Reorganization of a legal entity."

Reflect the amount of the authorized capital at the end of the reporting year on line 3300. This includes the credit balance of account 80 “Authorized capital” as of the end of the year.

Column 4 "Own shares purchased from shareholders"

This column reflects the value of shares that are purchased by the company from shareholders at their request or by decision of the board of directors.Limited liability companies reflect the value of shares in the authorized capital purchased from the participants (founders) of the company.

Column 5 "Additional capital"

Column 5 reflects data on the movement of the company’s additional capital.It changes, for example, as a result of the revaluation of fixed assets. To fill out column 5, use the data reflected in account 83 “Additional capital”.

First, give the amount of additional capital at the end of the year that preceded the previous year (reporting year minus two years).

Then, in the lines “Revaluation of property,” indicate the amount of increase or decrease in additional capital after the revaluation of the company’s property.

Write down the final amount of capital (including revaluation) in line 3300.

Reflect the amount of the company’s additional capital at the end of the last year, that is, 2015, in line 3200.

In the next line - 3312 - show the amount of the increase in additional capital from the revaluation of property carried out at the end of the reporting year, that is, 2016.

If, as a result of revaluation, additional capital decreased, then write down the amount of the decrease in line 3322.

On lines 3213 and 3313 “Income attributable directly to the increase in capital”, show the amount of VAT transferred to your company by the participant (shareholder) when paying for their shares (shares) in non-cash.

In accounting for this operation, the corresponding entry is Debit 19 Credit 83.

Reflect the amount of additional capital at the end of the reporting year in the final line 3300. This is the balance in account 83 “Additional capital” at the end of the reporting year.

Column 6 "Reserve capital"

The firm's reserve capital is formed from retained earnings.All joint stock companies are required to do this.

In this case, the amount of reserve capital must be at least 5% of the authorized capital (clause 1, article 35 of the Law of December 26, 1995 N 208-FZ).

This means that the charter of a joint stock company can provide for reserve capital in a larger amount.

Limited liability companies are not required to create a reserve fund.

But at the request of the founders, enshrined in the charter and reflected in the accounting policies, such companies can also create a reserve fund.

Account 82 “Reserve capital” is used to account for it. Therefore, to fill out column 6 “Reserve capital” of the report, use data on transactions on this account.

Information on changes in reserve capital in the report is also provided for two years and is reflected similarly to authorized and additional capital.

Column 7 "Retained earnings (uncovered loss)"

Here they reflect information about the movement of retained earnings (uncovered losses) of the company.It is formed from the profit remaining after paying income tax and contributions to reserve capital.

To fill out column 7, use the data from account 84 “Retained earnings (uncovered loss).”

If the company’s accounting policies changed during the previous and reporting years, this should affect the amount of retained earnings (clauses 14 and 15 of PBU 1/2008).

It should be noted that in 2016, there were no changes in regulatory legal acts that entailed the need to revise accounting policies.

In the lines “Revaluation of property”, show the amount of retained earnings from the revaluation of fixed assets, intangible assets and exploration assets.

When non-current assets are disposed of, the amount of their revaluation is transferred from additional capital to the company's retained earnings.

In the final line 3300, show the credit balance of account 84 at the end of the reporting period.

Column 8 "Total"

The indicators in this column are calculated.To fill it out, summarize the data in columns 3 to 7, inclusive, for each line of the report.

Adjustment due to changes in accounting policies and correction of errors

In Sect. 2 statements reflect adjustments to equity as of December 31:- the year preceding the reporting year (last year);

- the year preceding the previous one (the year before last).

First, indicate the amount of capital before adjustments (line 3400).

Then they reflect the amount of adjustment due to changes in accounting policies (line 3410) and correction of errors (lines 3420).

After this, the amount of capital after adjustment is calculated (line 3500).

Lines 3401 - 3502 provide a breakdown of data on retained earnings (uncovered loss) and other capital items for which the adjustment is made.

Net assets

In Sect. 3 of the report provides information on the size of the company's net assets as of December 31:- reporting year;

- previous (last) year;

- the year preceding the previous one (the year before last).

In other words, net assets are the value of the current and non-current assets of the enterprise, secured by its own funds.

In addition to filling out the statement of changes in capital, the amount of net assets is also needed:

- to control the size of the authorized capital;

- to determine the estimated share price.

The procedure for filling out individual lines of the Statement of Changes in Capital

It depends on whether you made adjustment entries to account 84 in the reporting year, i.e. such entries that are associated with changes in accounting policies or correction of significant errors (Letter of the Ministry of Finance dated January 27, 2012 N 07-02-18/01 ) .Option 1: You did not make any adjusting entries.

In this case, fill out lines from 3100 “Capital value as of December 31 of the year preceding the previous year” to 3200 “Capital value as of December 31 of the previous year” according to last year’s reporting data.

Lines starting with 3310 "Increase in capital - total" by 3300 “Capital value as of December 31 of the reporting year”, fill in according to accounting data.

If in the reporting year you received:

- profit, then in the column “Retained profit (uncovered loss)” of line 3311 “Net profit” indicate the credit turnover for the reporting year in account 84 in correspondence with account 99 “Profits and losses”;

- loss, then in the column “Retained earnings (uncovered loss)” of line 3321 “Loss” indicate the debit turnover for the reporting year on account 84 in correspondence with account 99.

- revaluation, then calculate the indicator in the column “Additional capital” of line 3312 “Revaluation of property” using the formula:

- markdown, then calculate the indicator in the column “Additional capital” of line 3322 “Revaluation of property” using the formula:

In the column “Retained earnings (uncovered loss)” of line 3327 “Dividends”, indicate the total amount of debit turnover for account 84 in correspondence:

With subaccount 75-2 “Calculations for payment of income”;

With account 70 “Settlements with personnel for wages” in terms of settlements for the payment of dividends.

The indicators that you obtained as a result of filling out section. 1 “Movement of capital” on line 3300 “Amount of capital as of December 31 of the reporting year” must correspond to the accounting data as of December 31.

In particular, the following must match:

- data in the column "Authorized capital" - with an account balance of 80;

- data in the column “Own shares purchased from shareholders” - with account balance 81;

- data in the column "Additional capital" - from account balance 83;

- data in the column “Retained earnings (uncovered loss)” - from account balance 84.

In the lines of Sect. 2 “Adjustments due to changes in accounting policies and correction of errors” put dashes.

In line 3600 “Net assets”, indicate the amount of net assets as of December 31 of the reporting year, last year and the year before.

Option 2. You made adjustment entries.

In this case, start filling out the OIC from section. 2 "Adjustments due to changes in accounting policies and correction of errors."

In the statement of changes in equity, indicate the amount of the adjustment to retained earnings associated with the correction of the error:

- if the error was made last year - in the column “Change in capital due to net profit (loss)”, line 3421 “Adjustment due to correction of errors”;

- if the error was made in earlier periods - in the column “As of December 31 of the year preceding the previous one” of line 3421 “Adjustment due to correction of errors.”

For example, in the column "Retained earnings (uncovered loss)" line 3311 OIC for the last year the indicated value is 10 million rubles. In the OIC for the reporting year in the column “due to net profit (loss)” of line 3420 “adjustment due to correction of errors” 2 million rubles will be indicated in brackets. Then at the OIC for the reporting year in the column “Retained earnings (uncovered loss)”, line 3211, you must indicate the value of 8 million rubles. (10 million rubles - 2 million rubles).

Fill in lines 3310 - 3300 and 3600 as in option 1.

Example. Completing the statement of changes in capital

The organization prepares a statement of changes in capital for 2016.

The table shows the capital account balances.

Balance as of December 31, 2015 | Balance as of December 31, 2016 |

|||||

80 "Authorized capital" | ||||||

81 "Own shares (shares)" | ||||||

82 "Reserve capital" | ||||||

83 "Additional capital" | ||||||

84 "Retained earnings (uncovered loss)" | ||||||

Account 84 reflects:

- on a loan - accrual of net profit in the amount of RUB 1,000,000;

- by debit - distribution of profit for dividends in the amount of 500,000 rubles.

We transfer data from the Statement of Changes in Capital for the previous year to lines 3100 - 3200.

In section 2 we put dashes.

Statement of changes in equity for 2016(filling sample)

Appendix No. 2

to the Order of the Ministry of Finance of Russia

dated 02.07.2010 N 66n

Statement of changes in equity for 2016

1. Capital movement

Indicator name | Authorized capital | Own shares purchased from shareholders | Extra capital | Reserve capital | Retained earnings (uncovered loss) | ||

| Amount of capital | |||||||

|

16 Capital increase - total: | |||||||

| including: net profit | |||||||

| property revaluation | |||||||

| income related directly to increase capital | |||||||

| additional issue of shares | |||||||

| increase in nominal share price | |||||||

| reorganization of legal | |||||||

| Reduction of capital - total: | |||||||

| including: | |||||||

| property revaluation | |||||||

| expenses related directly to decrease capital | |||||||

| reduction in nominal share price | |||||||

| reduction in the number of shares | |||||||

| reorganization of legal | |||||||

| dividends | |||||||

| Change in additional capital | |||||||

| Change in reserve capital | |||||||

| Amount of capital |

The statement of changes in capital is a document that provides an explanation of the balance sheet. A standard form 3 of the statement of changes in capital has been developed; you can download form 3 of the financial statements at the end of the article. This form can be modified and modified to suit the needs of the organization. In this article we will look at how to fill out a report on changes in capital using the example of preparing a unified Form 3. You can download a sample of filling out a report, Form 3, of the financial statements for 2014 below. There you can also download a form for a statement of changes in capital.

Purpose of the statement of changes in equity

This report discloses detailed information on the movement of reserve and additional capital, and also reflects information on changes in the value of the company's retained earnings (in some cases, uncovered losses), and the share of its own shares that are repurchased from shareholders. This report indicates adjustments related to changes in the organization and correction of errors.

All organizations are required to submit a report form with the exception of insurance, budget, credit and small enterprises. The date of preparation of the report is considered to be the last calendar day of the reporting period.

Form No. 3 is submitted to the local tax authorities annually, no later than three months from the end of the reporting year. Along with the specified form, you must also submit. Since 2013, in addition to the tax inspectorate, annual financial statements must be submitted to the statistical authorities.

Along with Form 3, you also need to submit other reports:

- balance sheet (form 1) – ;

- statement of financial results (form 2) – ;

- cash flow statement (form 4) – .

Statement of changes in capital sample form 3

The form for the statement of changes in capital contains 3 sections and a “header”. The header of the report is filled out in the same way as a balance sheet or profit and loss statement. Form 3 reflects data for 3 years: the reporting year, the previous reporting year, and the previous year. Our sample report is completed for the reporting year 2014, that is, it presents information for 2014, 2013 and 2012.

Completing the first section “Capital Movements”

The first section of the form discloses complete information about the movement of the organization’s capital (authorized, reserve, additional), data on changes in retained earnings and the value of its own shares that were purchased from participants.

The information in this section is reflected for three years (the reporting year and the two previous ones), with the exception of cases when the company has been operating for less than three years.

The lines with codes indicate the reasons for the change in capital, and columns 3-8 contain capital items.

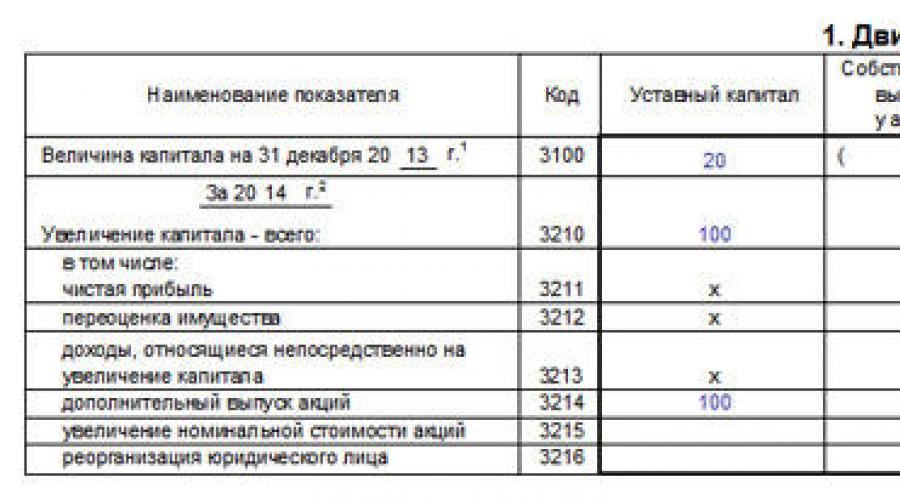

3100 reflects the credit balance (if the organization has uncovered losses, then the debit balance) for accounts 80, 81, 83, 82, 84 of accounting. The data is indicated for the year preceding the previous year before the reporting year (that is, for the year before last); when filling out Form 3 for 2014, this line reflects information for 2012 as of December 31.

Here page 3210 is filled in, after which below is a detailed transcript (3211-3216) of all business transactions that resulted in an increase in capital or retained earnings in the previous year.

Column 8 – summarizes the data for each line.

Thus, lines with codes 3211-3216 reflect credit turnover on accounts 80, 83, 82, 84.

3220 – data on the reduction of capital due to similar business transactions is reflected. Lines 3221-3227 form the debit turnover for accounts 80, 83, 82, 84. Their filling is similar to that indicated above.

Separately, codes 3230 and 3240 reflect changes in reserve and additional capital.

Line 3200 records the amount of the organization's capital, formed as the credit balance on accounts 80, 81, 83, 82, 84 as of the last day of the previous year.

Next, information for the reporting year is reflected, in our example for 2014. Lines 3310-3340 are filled in similarly to the previous year, data on increases and decreases in capital are also provided, and the amount of capital formed at the end of the reporting year is reflected in line 3300.

Completing the second section “Adjustments due to changes in accounting policies and correction of errors”

The second section of the report form reflects adjustments to the amounts of net profit (uncovered loss) and other items of equity that arose as a result of changes in accounting policies or correction of errors. The section is completed if the organization’s accounting policies have changed or errors in previous reporting periods have been corrected.

The third column of Form 3 includes the total amount of the enterprise's equity capital as of the end of the year preceding the previous one. 3400 displays the amount generated before adjustments, and 3500 – taking into account all subsequent changes. The amounts of adjustments as a result of changes in accounting policies or correction of errors are reflected in 3410 and 3420, 3400 and 3500 must be further deciphered: 3401-3501 are adjustments that changed the net profit figure, and 3402-3502 are other items of the reporting organization’s equity. The totals as of December 31 of the previous year are reflected in column No. 6.

Completing the third section “Net Assets”

The third section of the form (3600) reflects complete information about the organization’s net assets as of December 31 of the reporting year 2014, as of December 31 of the previous year and as of December 31 of the previous year. It is used by joint stock companies and limited liability companies. To calculate the amount of net assets, it is necessary to subtract the amount of liabilities accepted for calculation from the sum of all assets that are accepted for calculation.

Similar to other financial statements, negative data is given in parentheses on the statement of changes in equity form.

The statement of changes in capital can be completed in two versions:

- with line codes if reporting is submitted to statistical or other control structures;

- without specifying the line encoding if the document is intended for internal use (clause 5 of Order No. 66n).

This report form is needed to disclose detailed information about changes that have taken place in the institution in relation to the amount of equity capital. The reporting format involves reflecting data in three blocks:

- by type of capital;

- by type of change;

- with reference to years.

Form 3 of the report is designed for completion by legal entities. An exception is made for small businesses, insurance organizations, credit structures and budgetary institutions. As part of the annual reporting, the form is submitted to the regulatory authority within a three-month period from the end of the reporting year. The document is submitted to the tax authority with reference to the place of registration; reports must be submitted to the statistical authorities taking into account the place of registration of the legal entity.

Form 3 of financial statements: document structure and completion

Section 1 of the report shows systematic information on movements and balances on accounting accounts:

- 80 in relation to the authorized capital;

- 81 when disclosing details of transactions with own shares purchased from shareholders;

- 82 when reflecting the amount of reserve capital;

- 83 to identify additional capital;

- 84, used to account for undistributed profits or uncovered losses.

The statement of changes in capital (Form 3) in Section 1 has a two-part tabular part. The first block indicates the values of indicators for the previous period (they must coincide with the data indicated in block 2 of the table for the previous reporting period). The second part of the section is provided for information about the indicators of the last reporting period.

Section 2 discusses the amounts by which the cost of capital has been adjusted. The last tabular block of the report in Section 3 reflects information on the volume of net assets over time as of the end of December of the reporting year and the two previous years. How the size of net assets is determined is stated in the order of the Ministry of Finance No. 84n dated August 28, 2014:

- is the difference between the amount of assets on the balance sheet and the amount of liabilities;

- when calculating this indicator, amounts reflected in off-balance sheet accounts are not taken into account;

- the amounts of generated receivables of the founders in relation to contributions to capital or payment for shares are excluded from the assets;

- Liabilities do not include deferred income that was created as a result of receipt of government assistance or in the case of gratuitous transfer of property.

The capital flow statement is filled out only in monetary terms. Negative amounts are not accompanied by a minus sign; they are enclosed in parentheses. Empty columns must contain dashes. You can submit to regulatory authorities on paper or in electronic format. When reporting on paper, it is permitted to:

- submit the document in person;

- transfer to a tax authority specialist through a proxy;

- send by mail with the obligatory attachment of an inventory (the date of submission of the report will be considered the day of departure recorded by the post office).

The report form is prepared in two copies. Each of them is signed by the head of the organization. Art. 80 of the Tax Code of the Russian Federation establishes regulatory requirements for enterprises that must submit reports only in electronic form without the right to submit completed document forms in paper form.